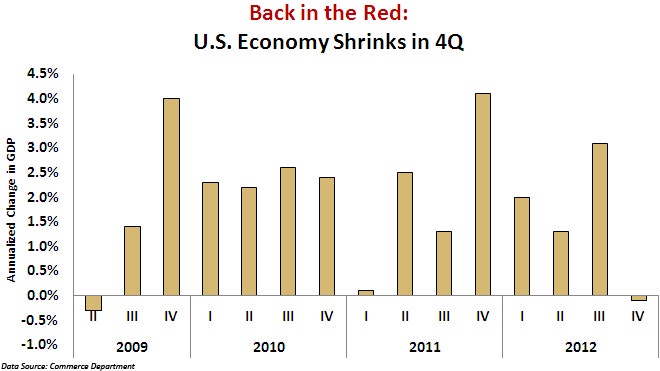

The U.S. economy unexpectedly contracted in the fourth quarter, suffering its first decline since the 2007-09 recession as businesses scaled back on restocking and government spending plunged.

Gross domestic product fell at a 0.1 percent annual rate after growing at a 3.1 percent clip in the third quarter, the Commerce Department said on Wednesday.

That was the worst performance since the second quarter of 2009, when the recession ended, and showed the economy entering the new year with no momentum.

The contraction, coming against a backdrop of tightening fiscal policy, could spur fears of a new recession and create an urgency for policymakers to deal with outstanding budget issues.

Economists polled by Reuters had expected output to increase at a 1.1 percent rate.

None of the economists surveyed had predicted a contraction.

A pick-up in consumer spending and a rebound in business investment, however, curbed the slide in output and offered some hope for the recovery, which will be severely tested as Washington tightens its belt.

The data was published as officials at the Federal Reserve wrap-up a two-day meeting. The report will likely provide ammunition for officials at the U.S. central bank to stay on their ultra-accommodative policy stance.

Economists say a growth pace in excess of 3 percent would be needed over a sustained period to significantly lower high unemployment. The economy has struggled to hold above a 2 percent growth pace.

For the whole of 2012 the economy grew 2.2 percent.

The economy was slammed by a monster storm in late October, which caused extensive damage along the East Coast, which was expected to have cut around 0.5 percentage point off fourth-quarter growth.

The recovery also had to deal with uncertainty over the so-called fiscal cliff of scheduled tax hikes and budget cuts, which hurt confidence even though data suggests that households and businesses largely shrugged off the worries.

SOME BRIGHT SIGNS

Businesses, caught with too much inventory in their warehouses in the third quarter, slowed their stock building in the final three months of the year.

That slowdown sliced 1.27 percentage points from fourth-quarter GDP growth. That was the biggest drag in two years. Excluding inventories, the economy grew at a 1.1 percent rate, slowing from the third quarter's 2.4 percent.

Government spending tumbled at a 6.6 percent rate, as defense outlays plunged at a 22.2 percent pace, wiping out the previous quarter's gains. Government subtracted 1.33 percentage points form growth. The decline in defense spending was the largest since 1972.

Export weakness also weighed on growth. Exports have been hampered by a recession in Europe, a cooling Chinese economy and storm and strike-related port disruptions. Overall trade cut a quarter of a percentage point from GDP growth. Exports fell for the first time since the first quarter of 2009.

But not all the details in the report were bleak.

Importantly, consumer and business spending showed some strength, and income available to households after taxes and inflation increased substantially in the fourth quarter.

Consumer spending, which accounts for more than two-thirds of economic activity, rose at a 2.2 percent rate, accelerating from the prior quarter's 1.6 percent growth pace.

Business investment rebounded after its first drop in 1-1/2 years in the prior quarter. The housing market was another bright spot. Residential construction grew at a 15.3 percent rate after notching a 13.5 percent growth pace in the third quarter.

Homebuilding added to growth last year for the first time since 2005.

(0)

(0) (0)

(0)