.jpg)

4) Spanish Mountain Gold - Update (May 1)

Spanish Mountain Gold - 运营更新

Spanish Mountain Gold - 運營更新

Barkerville, the legend of a once booming mining town in the Cariboo region, BC, located 50 Km north of Spanish Mountain Gold, started the world famous Cariboo gold rush.

https://www.google.ca/maps/dir/Barkerville,+B...FQAw%3D%3D

Video duration: 5 minutes

https://www.youtube.com/watch?v=XGfM7Ya1ulQ

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

As of Friday, May 1, the 25-cent warrant holders have only 19 trading days to exercise their 7,411,308 warrants which will expire on Friday, May 29, subject to early expiry if the 10-day average closing price exceeds 30 cents. Exercising of the warrants will provide the company additional $1.852 million.

Warrants, Options and Insider Share Ownership

https://investorshangout.com/images/MYImages/...302026.jpg

SPA.V weekly chart

https://stockcharts.com/sc3/ui/?s=SPA.V&p...2963243620

===================

Latest News Release

===================

As pledged by CEO Peter Mah, future financing will use non-dilutive approach, the royalty financing with Wheaton Precious Metals is a precedential example.

April 20, 2026 - Spanish Mountain Gold Announces Sale of a 1.5% Royalty to Wheaton Precious Metals for US$55 Million (approximately C$75 million)

https://spanishmountaingold.com/news/2026/spa...5-million/

May 1, 2026 - Spanish Mountain Gold Announces Closing of First Tranche of Royalty Financing and Receipt of US$22.5 Million (approximately C$30 million)

https://spanishmountaingold.com/news/2026/spa...5-million/

Highlights:

- The first installment of US$22.5 million has been closed and received from Wheaton.

- The second installment of US$12.5 million is payable to Spanish Mountain Gold following the completion of 60,000 meters of drilling at the Project.

- The third installment of US$20 million is payable to Spanish Mountain Gold on the receipt of approvals for the construction, development, and operation of a mine under the British Columbia Environmental Assessment Act.

WPM.TO weekly

https://stockcharts.com/sc3/ui/?s=WPM.TO&...8609492691

Wheaton Precious Metals website

https://www.wheatonpm.com/news/default.aspx

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

About Wheaton Precious Metals (WPM.TO)

Wheaton Precious Metals Corp. is the world's premier precious metals streaming company. Unlike traditional mining companies, Wheaton does not own or operate mines directly. Instead, it operates a "streaming" model, acting as a specialty financier that provides upfront capital to mining companies to construct or expand mines.

This is Wheaton's business model

https://www.wheatonpm.com/about/Our-Business-...fault.aspx

Streaming Agreements: In exchange for upfront financing, Wheaton acquires the rights to purchase a percentage of the future precious metal production (specifically gold, silver, palladium, and cobalt) from these mines at a low, fixed, or variable cost per ounce.

Asset Portfolio: Wheaton holds a high-quality portfolio of long-life, low-cost assets, with agreements on over 23 operating mines and 25 development projects globally.

Revenue Generation: The company generates revenue by selling the metals purchased through these streams, offering investors exposure to commodity price increases without the operational risks (capital expenditure, environmental, or political risk) associated with traditional mining.

Focus Areas: While they focus on precious metals, their agreements are often with large, multi-metal mines (like copper mines), where the precious metals are by-products.

Wheaton's dealing with Spanish Mountain Gold is 1.5% Royalty of the company's net revenue. The company's primary minerals are gold and silver. 2024 drilling program indicates that Portable XRF analysis identified potential for critical elements, including Titanium (Ti), Manganese (Mn), Magnesium (Mg), and Nickel (Ni). The company is analyzing this data and intends to investigate the potential for these elements as part of future exploration programs. There are also base metals such as galena, sphalerite, chalcopyrite, and pyrite.

Wheaton Precious Metals based in Vancouver, Canada was founded in 2004, it is a leader in the streaming sector.

Cash as of Dec 31, 2025: US$1.15 billion

Assets: US$1.2 billion

Liabilities: US$0.43 billion

2025 Sales: US$2.3 billion

2025 Cost of Sales: US$0.64 billion

Gross Profit Margin: US$1.67 billion

Net Earnings after Tax: US$1.47 billion

Basic Share Outstanding: 454,097,336

Earnings Per Share: US$3.24

PE Ratio: 60

Share Price: $198

Market Capitalization: $89.9 billion

==========================================

News on the progress of XRT ore sorting technology

==========================================

Spanish Mountain Gold has achieved highly positive results in Phase 1 XRT ore sorting tests for its Phoenix deposit, showing potential to double ROM feed grades while rejecting 50%–70% of waste mass. Tests show 85%–92% gold recovery, with Phase 2 bulk sample testing underway for a 2026 economic study. Following positive Phase 1 results, Phase 2 is evaluating 100-kg bulk samples in parallel with the Main deposit, aimed at optimizing sorting algorithms. The initiative aims to significantly reduce the size of the proposed mill and lower initial capital expenditure (CAPEX) for the project, with results likely to be incorporated into an updated economic assessment in 2026. Partners ABH Engineering Inc. and OrePortal Technologies Ltd. are working on particle and bulk sorting analysis. The company aims to make a construction decision in 2027 by enhancing project economics through enhanced feed grades.

==============

Coming events

==============

***** Metals Investor Forum (MIF) (May 8, 9 2026) at JW Marriott Parq Hotel, 39 Smithe St, Vancouver, BC V6B 0R3, Canada.

https://metalsinvestorforum.com/metals-investor-forum/

https://www.google.ca/maps/place/JW+Marriott+...FQAw%3D%3D

https://www.google.ca/maps/@49.2751365,-123.1...FQAw%3D%3D

***** A new PEA along with a new MRE from the 2025 Fall drill program will be released in May or June of 2026. The 2026 PEA will show significant reduction in Capital Expenditure in mine construction, significant increase in MRE and significant increase in gold grade feed to the mill.

***** Spanish Mountain Gold will be participating in the annual Mining Investment Event (THE Event) to be held on June 2 to June 4 in Quebec City, Quebec Province, Canada.

CEO Peter Mah presented Spanish Mountain Gold at the (June 3 - June 5) 2025 Mining Investment Event

https://www.youtube.com/watch?v=9MDABJPTEFU

***** 60,000-meter drill program, Feasibility Study, Construction Build Decision

Excerpt from Page 11 of MD&A of Dec 31, 2025 Annual Report : "The Company’s current strategy remains focused on optimizing, de-risking and advancing its Spanish Mountain Gold project towards a build decision before the end of 2027. With the completion of the 2025 PEA, the Company will be advancing directly to a Feasibility Study (“FS”). The Company requested proposals for conducting a Feasibility Study in Q4 2025 and recently awarded the lead to BBA Engineering Ltd. In the Interim, the Company, along with BBA, will be producing a PEA Update in H1 2026 (the first half of 2026) taking into account the potential addition of the Phoenix deposit mineralization, the 2025 Winter and Fall Drill Program results, the benefits of ‘ore’ sorting, and a higher long term gold forecast. The Company expects to drill at least 60,000 m over the next twelve months leading up to the production of the FS in 2027. This drilling will include geotechnical and hydrological drilling and test work necessary for designing the mill and tailing storage facilities."

https://spanishmountaingold.com/site/assets/f...4-2025.pdf

=================================================================

Spanish Mountain Gold is inching towards Feasibility and Mine Building Decision

=================================================================

Feb 27, 2026 - Spanish Mountain Gold Signs Memorandum of Understanding with Metso Canada Inc.

https://spanishmountaingold.com/news/2026/spa...anada-inc/

Metso Canada services (video)

https://www.youtube.com/watch?v=wgiF9uZqDsE

Metso Canada website

https://www.metso.com/corporate/sustainabilit...-offering/

Metso Canada (formerly Metso Outotec) is a technology provider that supplies mining equipment such as crushers and grinding mills to various companies, including recent project like Blackwater Mine in the Cariboo region of British Columbia. It is a leading global industrial company and a frontrunner in sustainable technologies, end-to-end solutions and services for the aggregates, minerals processing and metals refining industries. They focus on improving their customers’ energy and water efficiency, increase their productivity and reduce environmental risks with their product. Crushing, screening and grinding is their core business. Metso is headquartered in Espoo, Finland. At the end of 2025 Metso had close to 18,000 employees in around 50 countries, and sales in 2025 were about EUR 5.3 billion.

Key Aspects of Metso’s Business:

Aggregates: Provides crushing and screening equipment (mobile and fixed) for quarrying and construction industries.

Minerals Processing: Offers technology for mining, including grinding mills, separation, filtration, and tailings management.

Metals Refining: Provides solutions for metal processing.

Services & Wears: Delivers a broad portfolio of aftermarket services, spare parts, and wear parts to optimize equipment performance.

Sustainability: Focuses on "Planet Positive" solutions aimed at reducing energy and water consumption in customer operations.

==========================================================================

Spanish Mountain Gold - Vision For The Future ( following the footsteps of Blackwater Mine )

==========================================================================

Blackwater Mine - Owned by Artemis Gold, located 250 kilometers northwest of Spanish Mountain Gold and 160 km southwest of Prince George

Google Blackwater Mine map

https://www.google.ca/maps/place/Blackwater+M...FQAw%3D%3D

Artemis Gold share price ( ARTG.V )

https://stockcharts.com/sc3/ui/?s=ARTG.V&...8838982129

Blackwater Mine is an open pit gold and silver mine with mine life of 22 year and with scheduled mill throughput of 16,000 tpd, expandable to 33,000 tpd in year 6 and 55,000 tpd in year 11. The mine has Proven Reserves of 8 million ounces of gold, 62.2 million ounces of silver and Probable Resources of 11.7 million ounce of gold, 122.4 million ounces of silver.

In June, 2022 during the Phase 1 construction Metso delivered a Superior MK-III 4265 18MW primary gyratory crusher, HP900 cone crushers (secondary and tertiary), and a 14-MW Premier ball mill to Blackwater Mine. The delivery also included apron feeders, slurry pumps, hydrocyclones, and a RockSense particle size analyzer.

https://investorshangout.com/images/MYImages/...erMine.jpg

Phase 1 acquisition cost from Metso and construction cost is CAN$312 million, it included Engineering, Procurement, and Construction cost awarded to Sedgman.

Sedgman is a global leader in minerals processing and infrastructure solutions, offering end-to-end services from design and engineering to construction and operations. They specialize in coal, base/precious metals, and critical minerals, focusing on maximizing recovery, optimizing efficiency, and managing tailings for mining clients worldwide.

https://www.sedgman.com/

Artemis Gold also ordered C$134 million in primary mining equipment from Finning Canada for the Phase 1 development of the Blackwater Mine, representing a key component of the initial capital spending. This haul and load fleet includes Caterpillar trucks and excavators. Total Phase 1 project capital expenditure is estimated at C$730-C$750 million.

https://www.finning.com/en_CA.html

Mine construction began in 2023 and completed after 22-month with gold/silver pouring starting in early 2025. As one of Canada's largest gold development projects, it is a 100% electrified facility designed to be a low-emission, open-pit mine. The mine officially opened on May 30, 2025.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso Superior MK-III 4265 primary gyratory 18MW SAG mill crusher (breaks big ores into small ores)

https://www.youtube.com/watch?v=AVLicyiBLo8

The Metso Superior MKIII primary gyratory crusher is considered a significant innovation in mining, delivering up to 30% higher capacity and up to 70% less maintenance downtime than traditional crushers. It is marketed as the first high-speed primary gyratory crusher, featuring innovative digital automation, rotable shells for improved liner life, and superior capital efficiency. The gyratory crusher is a paradigm shift from the traditional ore crushing method.

How does a gyratory crusher work

https://www.youtube.com/watch?v=IYeOW7UCZAg&t=15s

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso Nordberg HP900 cone crusher (breaks small ores into pebbles)

https://www.youtube.com/watch?v=PRLCfhPudG8

How does a cone crusher work

https://www.foremanequipment.com/cone-crushers/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso 14MW ball mill (pulverizes pebbles to extract gold and silver particles)

https://youtu.be/4VmJ0vBRAG4

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Subsequent wet plant (milling and CIL circuit) transitioned the operation from construction to production.

The site features a fully electrified processing facility, a 225kV transmission line, and a significant tailings storage facility.

The project employs over 400 people, with a high percentage of local and Indigenous representation.

Designed with a low carbon footprint, replacing traditional fuels with electric equipment for mining and processing.

=================================

Blackwater Mine - Capital Expenditure

================================

The initial capital expenditure (CAPEX) for Phase 1 of the Blackwater Mine was estimated to be between C$730 million and C$750 million. As of December 31, 2023, approximately $389 million of this initial capital had been spent, with 84% of the lower end of the guided range ($615 million) contractually committed.

Remaining Capex: As of March 31, 2024, remaining Phase 1 capital expenditures were estimated at $207 to $227 million.

Scope: Phase 1 focused on building an open-pit mine and a processing facility with a capacity of 6 million tonnes per annum (Mtpa).

Subsequent Phase 1 Upgrades ("Phase 1A"

In September 2025, Artemis Gold announced plans to upgrade the Phase 1 processing plant (dubbed Phase 1A), aiming to increase capacity from 6 Mtpa to 8 Mtpa by Q4 2026.

Phase 1A Capital Cost: Estimated at $100 – $110 million, to be funded by operating cash flows.

Goal: To increase throughput and efficiency while leveraging the existing team that built Phase 1.

In December 2025 Artemis Gold approved a $1.44 billion Phase 2 expansion to increase production capacity from 8 million tonnes annually to 21 million tonnes annually. In March, 2026, Metso supplied a Superior MKIII primary gyratory crusher and Nordberg HP Series cone crushers to Blackwater Mine with a total value of approximately EUR 39 million (CAN$45.25 million, US$42 million). Construction is planned for Q3 2026 and is expected to be completed before the end of 2028. The expansion cost will be funded primarily through operating cash flows. Gold production will increase to over 500,000 ounces annually for the first 10 years.

https://artemisgoldinc.com/news/media-release...water-mine

==============================================

Blackwater Mine - Average gold grade and silver grade

==============================================

First 5 Years: Averaging 1.29 g/t gold.

Subsequent 17 years: Average 0.75 g/t gold.

Silver Grade: The average silver grade is estimated to be 5.78 g/t Ag over the life of the mine.

Reserve Basis: Total proven and probable reserves are estimated at 334.3 million tonnes at 0.75 g/t gold with gold content of 8 million ounces and 5.8 g/t silver with silver content of 62 million ounces.

First 5 years average annual production: 463,000 ounces of gold and 1.9 million ounces of silver.

=========================================================================

Blackwater Mine 2025 Average Realized Sale Price of gold. AISC and Net Production Profit

=========================================================================

Blackwater has capped off its inaugural operating year with record quarterly production of 68,480 ounces of gold during the three months ended December 31, 2025 (“Q4 2025”), bringing full year 2025 production to 192,808 ounces of gold. The quarterly gold production represents a 12% increase from the previous quarter and was primarily driven by higher mill feed grades and higher processing recoveries.

https://www.artemisgoldinc.com/news/artemis-g...6-guidance

https://www.artemisgoldinc.com/news/media-rel...ng-results

Based on financial results released by Artemis Gold, 2025 Average Realized Sale Price of gold is US$3,684 per ounce (C$5,095 per ounce).

2025 Q4 Average Realized Sale Price of gold is higher at US$4,168 per ounce (C$5,764 per ounce).

All-In-Sustaining-Cost (AISC) is US$869 per ounce (C$1,200 per ounce).

Blackwater Mine's 2025 Net profit is C$5095 - C$1200 = C$3895 per ounce gold produced

2025 total gold production is 192,808 ounces

2025 Net Production Profit is C$3895 per ounce x 192,808 ounces = C$750 million

April 9, 2026 - Artemis Gold announces Blackwater Mine produced 61,923 ounces of gold in Q1 2026. The plant processed 1.32 million tonnes and feed grades remained strong averaging 1.59 g/t gold during the quarter. The Company is maintaining its full year production guidance of 265,000 to 290,000 ounces of gold and is continuing to advance the Phase 1A expansion and the Expanded Phase 2 projects from operating cash flow. Annual throughput will increase to 21 million tonnes annually before the end of 2028, tripling the current capacity and increasing annual gold production to over 500,000 ounces.

==============================

Blackwater Mine construction videos

==============================

1) Feb 2025 - Aerial tour

https://www.youtube.com/watch?v=ndcRuX42b3U

2) Feb 2025 - Mining Technology

https://www.youtube.com/watch?v=8WfAvX_Nzb4

3) Feb 2025 - Health and Safety

https://www.youtube.com/watch?v=ELbEBpNQMAw

4) Feb 2025 - Completion of construction

https://www.youtube.com/watch?v=fpl3Vjd9slM

5) April 2025 - First gold pouring occurred in January 2025

https://www.youtube.com/watch?v=E9nFlVjKIe4

6 May 30, 2025 - Opening ceremony

https://www.youtube.com/watch?v=MOXjjZcGdYw

7) Dec 2025 - Phase 2: Production Expansion

https://www.youtube.com/watch?v=R7xr4kidz4I

==============================================================

Spanish Mountain Gold - Vision for the future through the life of Gibraltar Mines

==============================================================

https://www.youtube.com/watch?v=yJmanh1uQMQ

Gibraltar Mines - Owned by Taseko Mines, located 50 kilometers west of Spanish Mountain Gold

https://www.google.ca/maps/place/Gibraltar+Mi...FQAw%3D%3D

The Gibraltar Mine is the second-largest open-pit copper-molybdenum mine in Canada, owned and operated by Taseko Mines. Its primary resource is low-grade porphyry copper-molybdenum deposit containing minerals chalcopyrite, molybdenite, bornite, and cuprite. As of December 31, 2024, the mine has 616 million tons of 0.26% copper and 0.008% molybdenum.

https://stockcharts.com/sc3/ui/?s=TKO.TO&...5512188236

=========================================

Spanish Mountain Gold - Corporate Presentation

=========================================

https://spanishmountaingold.com/investors/presentations/

=============

Future Prospect

=============

Spanish Mountain Gold's market capitalization is well below its peer. With analysts providing price targets suggesting it is undervalued, potentially offering significant growth. The company's undervaluation stems from factors like a pending resource update, potential high-grade discoveries, and a unique "green gold" opportunity from available hydroelectric power.

Upcoming Catalyst: A new preliminary economic assessment and new resource estimate are expected to re-evaluate the stock's price.

Mineralization Potential: The project has high-grade mineralization across a significant length, suggesting the potential for future discoveries.

Green Gold Opportunity: The company's access to clean hydroelectric power presents a unique "green gold" investment prospect.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

CFO Mark Ruus presents Spanish Mountain Gold at VRIC on January 26, 2026 (Duration: 13 minutes)

https://www.youtube.com/watch?v=YzmLGz1Xhhg

Mark Ruus, Chief Financial Officer of Spanish Mountain Gold

Mr. Ruus brings nearly three decades in the mining sector. He began his career at PwC and has since progressed to Vice President and Senior Vice President Tax positions at leading gold mining firms like Kinross Gold Corporation, Goldcorp Inc., and Placer Dome Inc. His experience and CPA - CA qualification underpin his extensive knowledge in financing, cost control, business efficiency, compliance, tax issues, mergers and acquisitions, and financial reporting for domestic and global mining companies.

=================================

Spanish Mountain Gold's Strategic Shift:

=================================

Auditor Change and Leadership Transition as Catalysts for Growth in 2026.

- Spanish Mountain Gold replaces auditor and appoints new finance director to strengthen governance for 2027 construction decision.

- New auditor BDO and Kim Leroux’s expertise aim to enhance financial oversight and First Nations engagement in British Columbia.

- Operational readiness includes updated resource estimates, 2025 drilling, and XRT technology to optimize gold recovery and reduce carbon footprint.

- Strategic moves address governance risks and sustainability trends, positioning the company to navigate regulatory and market challenges.

The mining sector's transition from exploration to development-stage projects demands robust corporate governance and operational readiness. For Spanish Mountain Gold Ltd., a junior explorer aiming to evolve into an emerging developer, recent strategic moves-namely, a change in auditors and a leadership transition-signal a deliberate effort to align governance and technical capabilities with its 2027 construction decision timeline. These changes, coupled with operational advancements, position the company to navigate the complexities of project development in a resource-constrained and increasingly sustainability-focused industry.

Auditor Change: Strengthening Governance for Development-Stage Rigor

Spanish Mountain Gold's decision to replace Smythe LLP with BDO LLP as its auditor reflects a strategic pivot toward enhanced financial oversight and credibility. According to a report by Business Wire, the Audit Committee selected BDO for its "extensive experience working with mining companies," a critical factor as the firm advances its Spanish Mountain Gold Project toward a build decision. This shift underscores the company's recognition that development-stage projects require auditors with sector-specific expertise to navigate regulatory scrutiny and investor expectations.

The transition also highlights the importance of transparency in capital markets. By filing a Notice of Change of Auditor along with required letters from both the former and successor auditors on SEDAR+, Spanish Mountain Gold has demonstrated compliance with Canadian securities regulations. For investors, this move reduces governance risks associated with inexperienced auditors, a concern that has historically plagued junior miners. BDO's track record in mining audits may also facilitate smoother interactions with lenders and partners, who often demand rigorous financial due diligence before committing to large-scale projects.

Leadership Transition: Kim Leroux's Appointment as a Governance Win

Complementing the auditor change is the appointment of Kim Leroux as Director Finance, effective January 2, 2026. Leroux's background spanning roles at DeBeers and McEwen Mining Inc.-brings a depth of mining finance expertise that aligns with the company's operational ambitions. Notably, her experience in First Nations relationship management adds a critical dimension to corporate governance, particularly in British Columbia, where community engagement is pivotal to project permitting and social license to operate.

The transition from part-time contract CFO Mathew Lee to Leroux's full-time leadership role also addresses a common vulnerability in junior mining firms: inconsistent financial stewardship. By ensuring a seamless handover during Q1 2026, the company minimizes operational disruption while positioning itself to manage the capital-intensive phases of feasibility studies and infrastructure planning. Leroux's focus on "developing and implementing processes and systems" suggests a governance-driven approach to scaling operations, which is essential for attracting institutional investment.

Operational Readiness: Technical and Sustainability-Driven Progress

Beyond governance, Spanish Mountain Gold's operational readiness measures are equally compelling. The completion of a new Mineral Resource Estimate (MRE) and Preliminary Economic Assessment (PEA) by July 2025 provides a data-driven foundation for subsequent feasibility studies. These studies, combined with a 2025 exploration drill program targeting 10,000 meters, aim to de-risk the project by extending mineralization at key targets like Phoenix and K-zone.

Innovation in processing technology further strengthens the company's development-stage preparedness. The exploration of X-ray transmission (XRT) ore sorting-a technique to enhance gold recovery-demonstrates a proactive approach to optimizing project economics according to a Financial Post report. Simultaneously, collaborations with BC Hydro to integrate renewable diesel and electrification initiatives highlight a commitment to reducing the project's carbon footprint, a growing priority for ESG-focused investors. These efforts align with global trends toward decarbonization in mining, potentially improving the project's long-term viability in a regulatory and market landscape increasingly shaped by sustainability metrics.

Strategic Alignment and Future Outlook

Spanish Mountain Gold's dual focus on governance and operational readiness creates a synergistic foundation for its 2027 construction decision. The auditor change and leadership transition address internal capacity constraints, while technical advancements and sustainability initiatives tackle external challenges such as permitting delays and capital cost inflation. For development-stage miners, these factors are often the difference between project success and stagnation.

However, risks remain. The 2025 drill program's results will be critical in validating the MRE's assumptions, and delays in feasibility studies could push the construction decision beyond 2027. Additionally, Leroux's ability to integrate First Nations partnerships into the project's governance framework will determine the speed of regulatory approvals. Investors must monitor these milestones closely, but the company's current trajectory suggests a well-structured path to becoming a producer.

Conclusion

Spanish Mountain Gold's strategic shift in 2026-from auditor and leadership changes to operational innovations-exemplifies how development-stage mining firms can mitigate risks and enhance value. By prioritizing governance rigor and technical preparedness, the company is positioning itself to capitalize on the gold sector's long-term fundamentals while addressing the ESG imperatives of modern capital markets. For investors, the question is no longer whether the project can advance, but how swiftly it can execute its ambitious timeline.

News reference

https://spanishmountaingold.com/news/2025/spa...scal-2025/

==================================

Warrants, Options, Insider share ownership

==================================

https://investorshangout.com/images/MYImages/...302026.jpg

Insider trading transaction record

https://www.barchart.com/stocks/quotes/SPA.VN/insider-trades

https://www.canadianinsider.com/company-insid...cker=SPA.V

==========================================

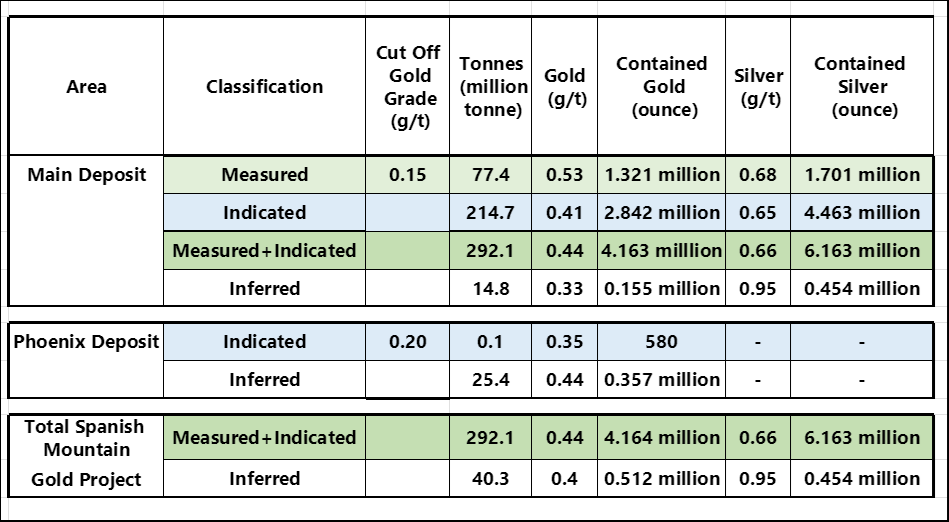

Mineral Resource Estimate (MRE) as of July 3, 2025

==========================================

https://investorshangout.com/images/MYImages/...timate.png

Resources in the high grade K-zones are not included in the July 3 PEA.

======================================

Unofficial gold resources estimate in the K-zone

======================================

As of March 10, 2026

https://investorshangout.com/images/MYImages/...K-zone.jpg

Drilling area:

https://investorshangout.com/images/MYImages/...argets.png

Based on the updated assays in the K-zone and based on the silver resource to gold resource ratio of 1.5 in the Main Zone, if the tonnage in the K-zone is at least 200 million tonnes as in the Main zone, K-zone will has Measured + Indicated resources of 4 million ounces gold and 6 million ounces silver added to the July 3, 2025 PEA. 2026 new PEA's new MRE will show gold and silver Measured + Indicated resources (Proven Reserve) of 8 million ounces of gold and 12 million ounces of silver.

2025 drilling consistently intersecting long intervals of high grade gold could be an indication that they are drilling close to the network of gold veins where the placer gold originated as some of the gold veins disintegrated and the gold fragments corroded into fine placer gold by weathering over millions of years. There could still be intact gold veins in SMG's 135 square kilometer property to be discovered. Including the high grade gold in future PEA will significantly reduce capital expenditure and increase gold productivity.

The term "high grade" is relative to the deposit style. The Spanish Mountain project is primarily a large-scale, open-pit, bulk-tonnage project, where the average grades are generally lower compared to narrow-vein underground mines. In this context, grades approaching or exceeding 1 g/t over significant widths are considered "higher-grade" and economically significant for the project's development, especially for the early years of the mine life. The company is also investigating ore sorting technology to potentially increase the processed grade and enhance project economics.

==================================

Charts - Gold, Silver, XAU, SPA.V, SPAUF

==================================

US Dollar Index

https://stockcharts.com/sc3/ui/?s=%24USD&...4982523747

Gold Price - weekly (price updated at End Of Day)

https://stockcharts.com/sc3/ui/?s=%24GOLD&...8609492691

50-year gold price

https://mrci.com/pdf/gc.pdf

Silver Price - weekly (price updated at End Of Day)

https://stockcharts.com/sc3/ui/?s=%24SILVER&a...8609492691

50-year silver price (price in cents)

https://mrci.com/pdf/si.pdf

XAU weekly

https://stockcharts.com/sc3/ui/?s=%24XAU&...4158123608

SPA.V weekly (In Canadian Dollar)

https://stockcharts.com/sc3/ui/?s=SPA.V&p...8609492691

SPA.V News, trade data

https://www.stockwatch.com/Quote/Detail.aspx?C:SPA.V

SPAUF.OTCQB weekly (In US Dollar)

https://stockcharts.com/sc3/ui/?s=SPAUF&p...8609492691

SPAUF Level 2

https://www.otcmarkets.com/stock/SPAUF/overview

S3Y.FSE (In Euro)

https://ca.finance.yahoo.com/quote/S3Y.F/char...NlcyI6e319

===============

Technical Analysis

===============

https://investorshangout.com/images/MYImages/...sition.png

https://investorshangout.com/images/MYImages/...M16yrs.jpg

https://investorshangout.com/images/MYImages/...alysis.png

=================

Vision for the future

=================

https://investorshangout.com/images/MYImages/...future.jpg

================================

Case history of bullish Head & Shoulder

================================

BullishHead&Shoulderpatternscasehistory.png)

https://investorshangout.com/images/MYImages/...istory.png

====================================

Production infrastructure build financing plans

====================================

Gold price

OPTION 1 - Joint venture with a cash rich mining company

OPTION 2A - Debt financing (With XRT ore sorting technology)

.jpg)

https://investorshangout.com/images/MYImages/...ology).jpg

OPTION 2B - Debt financing (No XRT ore sorting technology, process all rocks)

.jpg)

https://investorshangout.com/images/MYImages/...ology).jpg

OPTION 3 - Buyout deal

========================================

Historical buyout deals in the Golden Triangle, BC

========================================

Placer Dome and International Corona acquired Stikine Resources at Can$67 per share

https://www.northernminer.com/news/placer-sta...000178407/

Imperial Metals acquired American Bullion Minerals Ltd. at Can$2.45 a share

https://imperialmetals.com/for-our-shareholde...an-bullion

Newmont acquired GT Gold at $3.25 per share in a Can$393 million deal

https://www.newmont.com/investors/news-releas...fault.aspx

Australian gold and copper producer Newcrest Mining acquired Pretium Resources in a Can$3.84 billion, $18.5 per share deal

https://magazine.cim.org/en/news/2021/newcres...e%20region

In Ontario, Kinross acquired Great Bear Resources for $32 a share in the $1.8 billion deal

https://www.globalminingreview.com/finance-bu...resources/

====================================================

Preliminary Economic Assessment and NI-43-101 Technical Report

====================================================

https://investorshangout.com/images/MYImages/...67_PEA.png

Preliminary Economic Assessment Economics

https://spanishmountaingold.com/project/preli...economics/

August 18, 2025 - NI-43-101 Technical Report

https://spanishmountaingold.com/site/assets/f...-final.pdf

===================================

All-In-Sustaining-Cost of 25 gold producers

===================================

https://www.mining.com/wp-content/uploads/202...31425A.gif

What is All In Sustaining Costs (AISC)?

All-in Sustaining Costs (AISC) in the mining industry, particularly for gold, includes all operating costs, sustaining capital expenditures, and other costs associated with maintaining current production. This includes cash costs, sustaining capital expenditures, general and administrative (G&A) expenses, and environmental and closure costs.

Breakdown on AISC:

Cash Costs:

These are the direct costs of mining and processing, including labor, energy, consumables, and royalties (net of by-product credits).

Sustaining Capital Expenditures:

These are investments required to maintain current production levels, such as equipment replacement, mine development, and other costs to keep the mine operating at its current capacity.

General and Administrative (G&A) Expenses:

These are the costs associated with running the corporate office and other administrative functions that support the mine's operations.

Environmental and Closure Costs:

These include costs related to environmental remediation and mine closure, such as reclamation and decommissioning.

Exploration Expenses (Sustaining):

These are exploration costs that are needed to maintain current production levels and replace depleted resources.

AISC is a comprehensive metric designed to provide a more complete picture of the total cost of mining an ounce of gold, beyond just the direct cash costs.

===============================

Key Steps Leading to a Build Decision

===============================

Spanish Mountain Gold has indicated that production infrastructure construction decision will be made in 2026, after which a two-year construction phase will begin. This timeline allows for the completion of the ongoing drill program, a new Mineral Resource Estimate (MRE) and a new Preliminary Economic Assessment (PEA) in the second half of 2026, as well as securing all necessary reports and approvals to advance development of the project. The new PEA and MRE are crucial steps in optimizing the project for construction. Completing all technical reports and regulatory approvals is a necessary part of the process before the build decision can be made.

========

Overview

========

A mining project can pay loans before achieving revenue by using alternative financing like stream financing, royalty financing, or joint ventures, which are less restrictive than traditional debt and use future production or revenue as collateral instead of pre-existing income. Other methods include securing government grants and incentives, pre-selling a portion of future production through off-take agreements, and raising equity capital through share issues.

===========================

Pre-Revenue Financing Methods

===========================

Streaming Agreements: A company provides upfront capital in exchange for a percentage of the mine's future mineral production, often at a discounted price.

Royalty Financing: A financier funds a project in return for a share of the project's future revenue or profits, which can be seen as an endorsement of the project's potential.

Joint Ventures: Partnering with other mining companies or investors allows costs to be shared, spreading the financial burden, notes www.altfin.net.

Off-take Agreements: Pre-selling a portion of the future mineral output to buyers can secure upfront financing and provide lenders with confidence in the project's potential.

Government Funding: Governments and development banks sometimes offer grants, loans, or tax incentives for projects aligned with economic or environmental goals, according to www.altfin.net.

Equity Financing: Raising capital by issuing shares is often considered the simplest path for early-stage projects, as it avoids the complexities and strict requirements of debt financing.

Benefits of These Approaches

Non-Dilutive (for streams/royalties): These options don't dilute the original shareholders' equity in the company.

Flexible Terms: Stream and royalty structures can be more flexible and less restrictive than traditional bank debt, allowing for customized repayment profiles.

Market Confidence: Agreements like streaming and royalties can be seen as a market endorsement of the project, potentially leading to increased investor confidence.

===================

Promise for profitability

===================

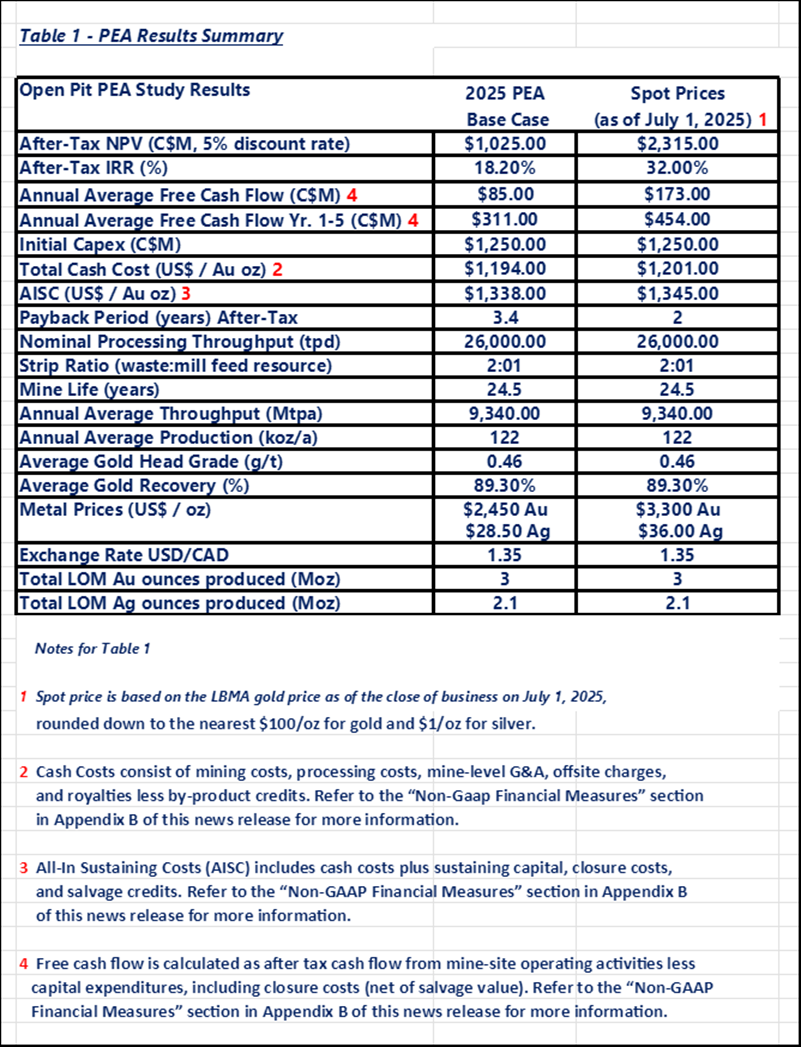

Spanish Mountain Gold shows promise for profitability due to a recently updated Preliminary Economic Assessment (PEA) indicating strong economics with a base case NPV5% of C$1.0 billion and an IRR of 18.2%, potentially improving to C$2.3 billion NPV5% and 32.0% IRR with higher gold prices. The project's conventional open-pit, milling operation, access to infrastructure, and new management team with experience in construction and operations contribute to its potential success, although the company is still in the early development stages.

Factors supporting profitability:

Favorable Economics: The PEA projects significant financial returns, with an after-tax Net Present Value (NPV) of C$1.0 billion and an Internal Rate of Return (IRR) of 18.2% at a base gold price of US$2,450/oz, and even better results at a spot price of US$3,300/oz gold.

Strong Resource Confidence: The economic analysis is based on a high degree of resource confidence, incorporating measured and indicated resources, which are key to a successful mining project.

Experienced Management: A new board and management team, brought in since 2022, possess decades of experience in project management, construction, and operations, positioning the company for a production decision.

Developed Infrastructure: The project will benefit from established infrastructure in central British Columbia, including road access and proximity to the city of Williams Lake, reducing operational complexities and costs.

Strategic Project Design: The company plans a conventional open-pit and milling operation, which is a low-risk approach that is less complex than underground mining.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

簡體中文

Barkerville 是位于 British Columbia Cariboo 地区 的一座曾经繁荣的矿业小镇,距离 Spanish Mountain Gold 以北50公里,它开启了举世闻名的Cariboo 淘金热。

https://www.google.ca/maps/dir/Barkerville,+B...FQAw%3D%3D

视频时长:5分钟

https://www.youtube.com/watch?v=XGfM7Ya1ulQ

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

截至5月1日星期五,每股面值 $0.25 的认股权证持有人仅剩19个交易日来行使他们持有的7,411,308份认股权证,这些认股权证将于5月29日星期五到期。如果10天平均收盘价超过 $0.30,则可能提前到期。行使这些认股权证将为公司带来额外的 $1.852 million。

认股权证、期权和内部人士持股

https://investorshangout.com/images/MYImages/...302026.jpg

SPA.V 周线图

https://stockcharts.com/sc3/ui/?s=SPA.V&p...2963243620

=============

最新新闻稿

=============

正如首席执行官 Peter Mah 所承诺的那样,未来的融资将采用非稀释性方式,与 Wheaton Precious Metals 的特许权使用费融资就是一个先例。

2026年4月20日 - Spanish Mountain Gold 宣布以 US$55 million (約 C$75 million)的价格向 Wheaton Precious Metals 出售 1.5% 的矿权使用费。

https://spanishmountaingold.com/news/2026/spa...5-million/

2026年5月1日 - Spanish Mountain Gold 宣布完成首期矿产资源融资并收到 US$22.5 million (約 C$30 million)

https://spanishmountaingold.com/news/2026/spa...5-million/

要点:

- 首期款项 US$22.5 million 来自 Wheaton 已完成支付.

- 项目完成 60,000 meters 钻探后,Spanish Mountain Gold 将收到第二笔款项 US$12.5 million.

- 项目获得 British Columbia 省环境评估法规定的矿山建设、开发和运营许可后,Spanish Mountain Gold 将收到第三笔款项 US$20 million。

WPM.TO 周报

https://stockcharts.com/sc3/ui/?s=WPM.TO&...8609492691

惠顿贵金属公司网站

https://www.wheatonpm.com/news/default.aspx

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

关于 Wheaton Precious Metals (WPM.TO)

Wheaton Precious Metals 是全球领先的贵金属流媒体公司。与传统矿业公司不同,惠顿并不直接拥有或运营矿山。相反,它采用“流媒体”模式,作为一家专业融资机构,为矿业公司提供前期资金,用于建设或扩建矿山。

这是惠顿的商业模式:

https://www.wheatonpm.com/about/Our-Business-...fault.aspx

流式交易协议:Wheaton 通过预付融资,获得从这些矿山购买未来一定比例贵金属产量(具体而言是黄金、白银、钯金和钴)的权利,购买价格可以是低廉的固定成本或浮动成本。

资产组合:Wheaton 拥有高质量的资产组合,这些资产寿命长、成本低,在全球范围内拥有超过23个运营矿山和25个开发项目的协议。

收入来源:公司通过出售通过这些流式交易购买的金属来获得收入,使投资者能够从商品价格上涨中获利,而无需承担传统采矿相关的运营风险(资本支出、环境风险或政治风险)。

重点领域:虽然 Wheaton 专注于贵金属,但他们的协议通常是与大型多金属矿山(例如铜矿)签订的,在这些矿山中,贵金属是副产品。

Wheaton 与 Spanish Mountain Gold 的协议是支付该公司净收入的1.5%作为特许权使用费。该公司主要矿产为黄金和白银。2024年的钻探计划显示,便携式X射线荧光光谱仪(XRF)分析表明,该矿藏可能蕴藏着包括钛(Ti)、锰(Mn)、镁(Mg)和镍(Ni)在内的关键元素。该公司正在分析这些数据,并计划在未来的勘探项目中进一步研究这些元素的潜力。此外,该矿藏还蕴藏着方铅矿、闪锌矿、黄铜矿和黄铁矿等贱金属。

Wheaton 成立于2004年,总部位于 Vancouver, 是流媒体领域的领军企业。

现金余额 (2025年12月31日):US$1.15 billion

资产:US$1.2 billion

负债:US$0.43 billion

2025年销售额: US$2.3 billion

2025年销售成本:US$0.64 billion

毛利润:US$1.67 billion

税后净利润: US$1.47 billion

流通股数量:454,097,336

每股收益: US$3.24

市盈率: 60

股价:C$198

市值:C$89.9 billion

========================

XRT矿石分选技术进展新闻

========================

Spanish Mountain Gold 在其 Phoenix 矿床 的第一阶段XRT矿石分选试验中取得了非常积极的成果,该技术有望将原矿(ROM)品位提高一倍,同时剔除50%至70%的废石。试验结果显示黄金回收率达到85%至92%,目前正在进行第二阶段的大宗样品测试,以期在2026年开展经济性研究。在第一阶段取得积极成果之后,第二阶段正在与主矿床并行评估100公斤的大宗样品,旨在优化分选算法。该计划旨在大幅缩小拟建选矿厂的规模,并降低项目的初始资本支出 (CAPEX),相关成果预计将于 2026 年纳入更新后的经济评估。合作伙伴 ABH Engineering Inc. 和 OrePortal Technologies Ltd. 正在进行颗粒和散装分选分析。公司计划通过提高矿石品位来提升项目经济效益,从而在 2027 年做出建设决策。

=========

近期活动

=========

***** 金属投资者论坛 (MIF)(2026 年 5 月 8 日至 9 日)将在加拿大 BC 省 Vancouver 的 JW Marriott Parq 酒店举行。39 Smithe St, Vancouver, BC V6B 0R3, Canada.

https://metalsinvestorforum.com/metals-investor-forum/

https://www.google.ca/maps/place/JW+Marriott+...FQAw%3D%3D

https://www.google.ca/maps/@49.2751365,-123.1...FQAw%3D%3D

***** 新的初步经济评估 (PEA) 以及 2025 年秋季钻探计划的新矿产资源估算 (MRE) 将于 2026 年 5 月或 6 月发布。2026 年的 PEA 将显示矿山建设资本支出大幅减少,矿产资源估算 (MRE) 大幅增加,以及选矿厂黄金原料品位大幅提高。

***** Spanish Mountain Gold 将参加于 6 月 2 日至 4 日在加拿大 Quebec 省 Quebec 市举行的年度矿业投资盛会 (THE Event)。

首席执行官 Peter Mah 在 2025年 矿业投资活动(6月3日至5日)上介绍了 Spanish Mountain Gold。

https://www.youtube.com/watch?v=9MDABJPTEFU

***** 60,000米钻探计划、可行性研究、施工决策

摘自2025年12月31日年度报告管理层讨论与分析第11页:“公司目前的战略重点仍然是优化、降低风险并推进其西班牙山金矿项目,力争在2027年底前做出建设决策。随着2025年初步经济评估(PEA)的完成,公司将直接进入可行性研究(FS)阶段。公司已就2025年第四季度开展可行性研究征求方案,并于近期将牵头单位授予 BBA Engineering Ltd.。在此期间,公司将与 BBA 合作,于2026年上半年 发布PEA更新报告,其中将考虑凤凰矿床矿化的潜在新增情况、2025年冬季和秋季钻探计划的结果、矿石分选的优势以及更高的长期黄金产量预测。公司预计在未来十二个月内至少钻探60,000米,直至项目投产。”预计于 2027 年进行可行性研究。此次钻探将包括选矿厂和尾矿库设计所需的地质技术和水文钻探及测试工作"。

https://spanishmountaingold.com/site/assets/f...4-2025.pdf

=================================================

Spanish Mountain Gold 正在逐步接近可行性和矿山建设决策

=================================================

2026年2月27日 - Spanish Mountain Gold 与 Metso Canada Inc.签署谅解备忘录

https://spanishmountaingold.com/news/2026/spa...anada-inc/

Metso Canada 服务(视频)

https://www.youtube.com/watch?v=wgiF9uZqDsE

Metso Canada 网站

https://www.metso.com/corporate/sustainabilit...-offering/

Metso Canada(前称Metso Outotec) 是一家技术供应商,为提供多家公司采矿设备例如破碎机和磨机, 包括位于 British Columbia Cariboo 地区 的 Blackwater Mine。作为一家全球领先的工业公司,Metso Canada 在骨料、矿物加工和金属精炼行业的可持续技术、端到端解决方案和服务方面处于领先地位。该公司致力于通过其产品提高客户的能源和水资源利用效率,提升生产率并降低环境风险。破碎、筛分和研磨是其核心业务。Metso 总部位于 Espoo, Finland。截至2025年底,Metso在全球约50个国家拥有近18000名员工,2025年的销售额约为 5.3 billion 欧元。

Metso业务的关键方面:

骨料:为采石和建筑行业提供破碎和筛分设备(移动和固定)。

矿物加工:提供采矿技术,包括磨矿机、分离、过滤和尾矿管理。

金属精炼:提供金属加工解决方案。

服务与磨损件:提供广泛的售后服务、备件和磨损件,以优化设备性能。

可持续性:专注于“积极地球”解决方案,旨在减少客户运营中的能源和水消耗。

=======================================================

Spanish Mountain Gold -- 展望未来 ( 追随Blackwater Mine 的足迹 )

=======================================================

Blackwater Mine - Artemis Gold 拥有,位于西班牙山黄金 以西250公里,Prince George 以西南160公里。

Google Blackwater Mine 地图

https://www.google.ca/maps/place/Blackwater+M...FQAw%3D%3D

Artemis Gold 股价 (ARTG.V)

https://stockcharts.com/sc3/ui/?s=ARTG.V&...8838982129

该矿为露天金银矿,矿山寿命为22年,选矿厂日处理量为16,000吨,可在第6年扩建至33,000吨,在第11年扩建至55,000吨。该矿已探明黄金储量为800万盎司,白银储量为6220万盎司;概略资源量为1170万盎司黄金,白银储量为1.224亿盎司。

2022年6月,为配合一期选矿厂,Metso 向 Blackwater Mine 交付了一台 Superior MK-III 4265型 18兆瓦一级旋回破碎机、HP900系列圆锥破碎机(二级和三级)以及一台 14兆瓦 Premier 球磨机。此次交付还包括板式给料机、泥浆泵、水力旋流器和 RockSense 粒度分析仪。

https://investorshangout.com/images/MYImages/...erMine.jpg

第一阶段运营成本为 312 million 加元,其中包括授予Sedgman公司的工程、采购和施工(EPC)费用。

Sedgman是全球领先的矿物加工和基础设施解决方案提供商,提供从设计、工程到施工和运营的全流程服务。他们专注于煤炭、贱金属/贵金属和关键矿物,致力于为全球矿业客户最大限度地提高回收率、优化效率并管理尾矿。

https://www.sedgman.com/

Artemis Gold 还向 Finning Canada 订购了价值 134 million 加元 Blackwater Mine 的第一期开发所需主要采矿设备,这是初期资本支出的重要组成部分。这批运输和装载设备包括卡特彼勒卡车和挖掘机,第一期项目总投资预计为 730 million 至 750 million 加 元。

https://www.finning.com/en_CA.html

矿山建设于2023年启动,历时22个月竣工,金银矿体于2025年初开始浇铸。作为加拿大最大的黄金开发项目之一,该矿采用100%电气化设计,旨在打造低排放的露天矿。矿山于2025年5月30日正式投产。

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Superior MK-III 4265 型一级旋回式 18MW SAG 磨机破碎机 (将大块矿石破碎成小块矿石)

https://www.youtube.com/watch?v=AVLicyiBLo8

Metso Superior MKIII一级旋回破碎机被认为是采矿领域的一项重大创新,与传统破碎机相比,其产能提升高达30%,维护停机时间减少高达70%。该破碎机作为首款高速一级旋回破碎机推向市场,采用创新的数字化自动化技术,配备可旋转的破碎筒体以延长衬板寿命,并具有卓越的投资效率。 旋回破碎机是传统矿石破碎方法的一次范式转变。

旋回破碎机的工作原理是什么?

https://www.youtube.com/watch?v=IYeOW7UCZAg&t=15s

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso Nordberg HP900 型圆锥破碎机 (将小块矿石破碎成卵石)

https://www.youtube.com/watch?v=PRLCfhPudG8

圆锥破碎机的工作原理是什么?

https://www.foremanequipment.com/cone-crushers/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso 14MW 球磨机 (将鹅卵石粉碎以提取金银颗粒)

https://youtu.be/4VmJ0vBRAG4

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

随后的湿法厂(磨矿和CIL工艺)将运营从建设阶段转变为生产阶段。

该地点设有一个完全电气化的加工设施、一条 225 kilovolt 的输电线和一个重要的尾矿储存设施。

该项目雇用了超过400人,其中有很高比例的本地和土著代表。

设计时考虑了低碳足迹,用电动设备替代传统燃料进行采矿和加工。

这是一个露天金银矿,矿山寿命为22年,矿厂处理量为每天 16,000吨,6年后可扩展至每天 33,000吨,11年后可扩展至每天 55,000吨。 它拥有 8 million 盎司的黄金、62,2 million 盎司的白银的探明储量,以及11.7 million 盎司的黄金、122.4 million 盎司的白银的可能资源。

=======================

Blackwater Mne - 资本支出

=======================

Blackwater Mine 第一阶段的初始资本支出(CAPEX)预计在 730 million 加元 至 750 million 加元之间。 截至2023年12月31日,约 389 million 加元的初始资本已被支出,其中 84% 的指导范围下限(615 million 加元)已合同承诺。

剩余资本支出: 截至2024年3月31日,第一阶段剩余的资本支出估计在 207 million 至 227 million 加元之间。

范围:第一阶段集中于建设一个露天矿和一个年处理能力为 6 million 吨的加工设施。

后续第一阶段升级(“第一阶段A”)

2025年9月,Artemis Gold宣布计划升级第一阶段处理厂(称为第一阶段A),目标是在2026年第四季度之前将产能从每年 6 million 吨提高到 8 million 吨。

第一阶段A资本成本:估计为 100 million 至 110 million 加元,由运营现金流资助。

目标:在利用建设第一阶段的现有团队的同时,提高产量和效率。

2025年12月,Artemis Gold批准了一项价值 1.44 billion 加元 的二期扩建项目,旨在将年产能从 8 million 吨提升至 21 million 吨。2026年3月,Metso 向 Blackwater Mine 提供了一台 Superior MKIII型 一级旋回破碎机和 Nordberg HP系列 圆锥破碎机,总价值约为 39 million 欧元(45.25 million 加元,42 million 美元)。该项目计划于2026年第三季度开工建设,预计将于2028年底前完工。扩建成本将主要通过运营现金流来支付。扩建后的前十年,黄金年产量将超过 500,000 盎司。

https://artemisgoldinc.com/news/media-release...water-mine

================================

Blackwater Mine - 平均金品位和银品位

================================

前五年:平均金品位 1.29 克/吨。

后十七年:平均金品位 0.75 克/吨。

银品位:预计矿山寿命期内平均银品位为 5.78 克/吨。

储量:探明和概略储量总计估计为 334.3 million 吨,金品位 0.75 克/吨,含金量 8 million 盎司;银品位 5.8 克/吨,含银量 62 million 盎司。

前五年平均年产量:黄金 463,000 盎司,白银 1.9 million 盎司

======================================================

Blackwater Mine 2025 年黄金平均实际售价, 维持成本, 生产净利润

======================================================

Blackwater Mine 在截至2025年12月31日的三个月内(“2025年第四季度”)创下季度黄金产量68,480盎司的纪录,为其首个运营年度画上了圆满的句号,使2025年全年黄金产量达到192,808盎司。该季度黄金产量较上一季度增长12%,主要得益于选矿厂进料品位和加工回收率的提高。

https://www.artemisgoldinc.com/news/artemis-g...6-guidance

https://www.artemisgoldinc.com/news/media-rel...ng-results

根据 Artemis Gold 发布的财务业绩,2025 年黄金平均实现售价为每盎司 3,684 美元(每盎司 5,095 加元)。

2025 年第四季度黄金平均实现售价比较高, 每盎司 4,168 美元(每盎司 5,764 加元)。

维持成本 (AISC) 为每盎司 869 美元(每盎司 1,200 加元)。

Blackwater Mine 2025年 净利润为每盎司黄金 5095 加元 - 1200 加元 = 3895 加元

2025年 黄金总产量为 192,808 盎司

2025年 生产净利润为每盎司 3895 加元 x 192,808 盎司 = 7.5 亿 加元

2026年4月9日 - Artemis Gold 宣布,Blackwater Mine 在2026年第一季度生产了61,923盎司黄金。该选矿厂处理了1.32 million 吨矿石,矿石品位保持强劲,平均品位为1.59克/吨。公司维持全年黄金产量预期为 265,000 至 290,000 盎司,并正利用运营现金流继续推进1A期扩建项目和2期扩建项目。到2028年底,年处理量将增至 21 million 吨,是目前产能的三倍,年黄金产量也将超过 500,000 盎司。

======================

Blackwater Mine 建设视频

======================

1) 2025年2月 - 空中巡游

https://www.youtube.com/watch?v=ndcRuX42b3U

2) 2025年2月 - 矿业技术

https://www.youtube.com/watch?v=8WfAvX_Nzb4

3) 2025年2月 - 健康与安全

https://www.youtube.com/watch?v=ELbEBpNQMAw

4) 2025年2月 - 完工

https://www.youtube.com/watch?v=fpl3Vjd9slM

5) 2025年4月 - 首次黄金浇铸于2025年1月进行

https://www.youtube.com/watch?v=E9nFlVjKIe4

6) 2025年5月30日 - 开幕式

https://www.youtube.com/watch?v=MOXjjZcGdYw

7) 2025年12月 - 第二阶段:生产扩展

https://www.youtube.com/watch?v=R7xr4kidz4I

===================================================

Spanish Mountain Gold - 通过 Gibraltar Mines 的一生未来展望

===================================================

https://www.youtube.com/watch?v=yJmanh1uQMQ

Gibraltar Mines - 隶属于 Taseko Mines, 位于西班牙山金矿以西50公里处

https://www.google.ca/maps/place/Gibraltar+Mi...FQAw%3D%3D

Gibraltar Mines 是加拿大第二大露天铜钼矿,其主要资源为低品位斑岩型铜钼矿床,矿物成分包括黄铜矿、辉钼矿、斑铜矿和赤铜矿。截至2024年12月31日,该矿拥有6.16亿吨矿石,铜品位为0.26%,钼品位为0.008%。

https://stockcharts.com/sc3/ui/?s=TKO.TO&...5512188236

=============================

Spanish Mountain Gold - 公司介绍

=============================

https://spanishmountaingold.com/investors/presentations/

==========

未来展望

==========

Spanish Mountain Gold 市值远低于同行。分析师给出的目标价表明该公司被低估,具有巨大的增长潜力, 原因包括即将发布的资源量更新报告、潜在的高品位矿藏发现,以及利用现有水力发电资源开发独特的“绿色黄金”机遇。

即将到来的催化剂:新的初步经济评估和资源估算预计将重新评估该股的价格。

矿化潜力:该项目拥有覆盖广泛、品位高的矿化带,表明未来存在发现金矿的潜力。

绿色黄金机遇:该公司拥有清洁水力发电的渠道,为其带来了独特的“绿色黄金”投资前景。

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

首席财务官 Mark Ruus 介绍 Spanish Mountain Gold 2026 年 1 月 26 日在 VRIC 举办(时长:13 分钟)

https://www.youtube.com/watch?v=YzmLGz1Xhhg

Mark Ruus 在矿业领域拥有近三十年的从业经验。他最初在普华永道 (PwC) 工作,之后在 Kinross Gold Corporation、Goldcorp Inc. 和 Placer Dome Inc. 等领先的黄金矿业公司担任副总裁和高级副总裁税务职位。他丰富的经验和注册会计师 (CPA-CA) 资格,使其在国内外矿业公司的融资、成本控制、业务效率、合规、税务问题、并购和财务报告方面拥有广泛的知识。

==============================

Spanish Mountain Gold 的战略转变

==============================

审计师更换和领导层过渡作为2026年增长的催化剂

- Spanish Mountain Gold 更换审计师并任命新财务总监,以加强2027年建设决策的治理

- 新审计师 BDO 和 Kim Leroux 的专业知识旨在加强不列颠哥伦比亚省的财务监督和原住民参与。

- 运营准备包括更新的资源估算、2025年的钻探以及XRT技术,以优化黄金回收并减少碳足迹。

- 战略举措应对治理风险和可持续发展趋势,使公司能够应对监管和市场挑战。

采矿行业从勘探阶段过渡到开发阶段项目需要强有力的公司治理和运营准备。 对于 Spanish Mountain Gold 来说,这家初级勘探公司旨在发展成为新兴开发商,最近的战略举措——即更换审计师和领导层过渡——表明其有意努力将治理和技术能力与2027年的建设决策时间表对齐。 这些变化,加上运营方面的进展,使公司能够在资源受限且日益注重可持续发展的行业中,驾驭项目开发的复杂性。

审计师更换:加强发展阶段的治理严谨性

Spanish Mountain Gold 决定将 Smythe LLP 更换为 BDO LLP 作为其审计师,反映出其在财务监督和信誉方面的战略转变。 根据Business Wire的一份报告,审计委员会选择了 BDO,因为其“在与矿业公司合作方面拥有丰富经验”,这是该公司在推进其西班牙山金矿项目至建设决策时的一个关键因素。 这一转变突显了公司认识到开发阶段项目需要具备行业专业知识的审计师,以应对监管审查和投资者期望。

这一过渡也突显了资本市场透明度的重要性。 通过在 SEDAR+ 上提交更换审计师通知以及前任和继任审计师的必要函件,西班牙山黄金 展示了其遵守加拿大证券法规的合规性。 对于投资者来说,这一举措减少了与缺乏经验的审计师相关的治理风险,这是历史上困扰初级矿业公司的一个问题。 BDO 在矿业审计方面的良好记录也可能促进与贷款人和合作伙伴的更顺畅互动,这些贷款人和合作伙伴在承诺大型项目之前通常要求进行严格的财务尽职调查。

领导层过渡:Kim Leroux 的任命是治理的胜利

与审计师更换相辅相成的是 Kim Leroux 被任命为财务总监,任命将于2026年1月2日生效。 Leroux 在 DeBeers 和 McEwen Mining Inc.的背景带来了深厚的矿业金融专业知识,这与公司的运营目标相一致。 值得注意的是,她在第一民族关系管理方面的经验为公司治理增添了一个关键维度,特别是在不列颠哥伦比亚省,在那里社区参与对项目许可和社会运营许可证至关重要。

从兼职合同首席财务官 Mathew Lee 过渡到 Leroux 的全职领导角色,也解决了初级矿业公司常见的一个弱点:财务管理不一致。 通过确保在2026年第一季度进行无缝交接,公司在最小化运营中断的同时,也为管理资本密集型的可行性研究和基础设施规划阶段做好了准备。 勒鲁对“开发和实施流程和系统”的关注表明了一种以治理为驱动的扩展运营的方法,这对于吸引机构投资至关重要。

运营准备:技术和可持续性驱动的进展

除了治理之外,Spanish Mountain Gold 的运营准备措施同样引人注目。 到2025年7月完成新的矿产资源估算(MRE)和初步经济评估(PEA)为后续的可行性研究提供了数据驱动的基础。 这些研究结合了2025年的勘探钻探计划,目标是10,000米,旨在通过在凤凰区和K区等关键目标地延伸矿化来降低项目风险。

加工技术的创新进一步增强了公司在开发阶段的准备。 根据《金融邮报》的报道,探索X射线透射(XRT)矿石分选技术——一种提高黄金回收率的技术——展示了优化项目经济性的积极方法。 同时,与 BC Hydro 的合作整合可再生柴油和电气化举措,突显了减少项目碳足迹的承诺,这已成为以 ESG 为重点的投资者日益关注的优先事项。 这些努力与全球矿业去碳化的趋势相一致,可能会在一个日益受到可持续性指标影响的监管和市场环境中,改善项目的长期可行性。

战略对齐与未来展望

Spanish Mountain Gold 在治理和运营准备方面的双重关注为其2027年的建设决策奠定了协同基础。 审计师更换和领导层过渡解决了内部能力限制,而技术进步和可持续发展举措则应对了外部挑战,如许可延误和资本成本通胀。 对于处于开发阶段的矿业公司来说,这些因素往往是项目成功与停滞之间的关键区别。

然而,风险仍然存在。 2025年的钻探计划结果将对验证矿产资源估算(MRE)的假设至关重要,而可行性研究的延迟可能会将建设决策推迟到2027年以后。 此外,Leroux将原住民合作伙伴关系整合到项目治理框架中的能力将决定监管审批的速度。 投资者必须密切关注这些里程碑,但公司的当前轨迹表明其成为生产商的道路结构良好。

结论

Spanish Mountain Gold 在2026年的战略转变从审计和领导层变动到运营创新展示了开发阶段的矿业公司如何减轻风险并提升价值。 通过优先考虑治理严格性和技术准备,公司正在为利用黄金行业的长期基本面做好准备,同时应对现代资本市场的ESG要求。 对于投资者来说,问题不再是项目能否推进,而是它能多快执行其雄心勃勃的时间表。

新闻参考

https://spanishmountaingold.com/news/2025/spa...scal-2025/

====================================

截至2025年7月3日的矿产资源量估算 (MRE)

====================================

https://investorshangout.com/images/MYImages/...timate.png

高品位K区矿床的资源量未包含在7月3日的初步经济评估 (PEA) 中。

=========================

K区非官方估算的黄金资源量

=========================

截至3月10日

https://investorshangout.com/images/MYImages/...K-zone.jpg

钻井区域:

https://investorshangout.com/images/MYImages/...argets.png

根据 K 区更新的化验结果,以及主矿区白银资源量与黄金资源量之比为 1.5,如果K区的吨位至少达到2亿吨,与主区相同,K 区在 2025 年 7 月 3 日的初步经济评估中将新增 4 million 盎司黄金和 6 million 盎司白银的探明 + 指示资源量。2026 年新的初步经济评估报告 (PEA) 的新矿产资源估算报告 (MRE) 将显示已探明和已指示的黄金和白银资源量(已证实储量)分别为 8 million 盎司黄金和 12 million 盎司白银。

2025年的钻探工作持续发现长段高品位金矿表明我们钻探的区域可能靠近金矿脉网络,而砂金的来源正是这些金矿脉。这些金矿脉在两亿年的风化作用下崩解,可见的金被腐蚀成细小的砂金。将高品位金矿纳入未来的初步经济评估将显著改善项目的经济效益。

“高品位”一词的含义取决于矿床类型。西班牙山项目主要是一个大型露天矿项目,其矿石品位通常低于窄脉地下矿。在此背景下,品位接近或超过1克/吨且矿体宽度较大的矿石被视为“高品位”,对项目开发具有重要的经济意义,尤其是在矿山运营初期。公司目前也在研究矿石分选技术,以期提高矿石品位,从而提升项目经济效益。

===================================

图表 - 黄金、白银、XAU、SPA.V、SPAUF

===================================

美元指数

https://stockcharts.com/sc3/ui/?s=%24USD&...4982523747

黄金价格 周线图 (价格仅在每日收盘时更新)

https://stockcharts.com/sc3/ui/?s=%24GOLD&...8609492691

白银价格 周线图 (价格仅在每日收盘时更新日)

https://stockcharts.com/sc3/ui/?s=%24SILVER&a...8609492691

矿业指数 (XAU) 周线图

https://stockcharts.com/sc3/ui/?s=%24XAU&...4158123608

SPA.V 周线图 (加元)

https://stockcharts.com/sc3/ui/?s=SPA.V&p...8609492691

SPA.V - 新闻、交易数据

https://www.stockwatch.com/Quote/Detail.aspx?C:SPA.V

SPAUF.OTCQB 周线图 (美元)

https://stockcharts.com/sc3/ui/?s=SPAUF&p...8609492691

SPAUF 二级

https://www.otcmarkets.com/stock/SPAUF/overview

S3Y.FSE (欧元)

https://ca.finance.yahoo.com/quote/S3Y.F/char...NlcyI6e319

=========

技术分析

=========

https://investorshangout.com/images/MYImages/...sition.png

https://investorshangout.com/images/MYImages/...M16yrs.jpg

https://investorshangout.com/images/MYImages/...alysis.png

=============================

Spanish Mountain Gold - 未来展望

=============================

https://investorshangout.com/images/MYImages/...future.jpg

================

看涨头肩形态案例

================

https://investorshangout.com/images/MYImages/...istory.png

=========

勘探潜力

=========

Spanish Mountain Gold 近期钻探工作持续发现长段金矿化,其中包括显著的高品位矿段,其品位通常高于项目整体平均品位。公司正重点勘探并确认这些高品位矿化区域,以期提升项目经济效益。

金品位及矿段详情

项目整体品位:2025年初步经济评估(PEA)中,已探明和已控制矿产资源的平均品位约为0.44克/吨。

高品位矿段:近期勘探钻探计划旨在确定可纳入未来矿山规划的高品位矿化带。这些勘探项目已取得多个显著的高品位矿段:

其中一个钻孔截获了123.00米、平均金品位为1.08克/吨的矿段,其中包括一段47.28米、平均金品位为2.29克/吨的高品位矿段。

另一个钻孔截获了一段107.50米、平均金品位为0.68克/吨的矿段,其中包括一段41.00米、平均金品位为0.98克/吨的矿段。

钻探还证实,在一段更宽的96.47米、平均金品位为0.91克/吨的矿段内,存在一段29.00米、平均金品位为2.55克/吨的连续高品位矿段。

在新的 Orca 断层区域进行的近地表钻探也显示出多处长截矿段,例如35.80米、金品位1.18克/吨和41.00米、金品位0.98克/吨。

“高品位”的定义

“高品位”一词与矿床类型相关。Spanish Mountain Gold 项目主要是一个大型露天矿项目,其平均品位通常低于窄脉地下矿。在此背景下,品位接近或超过1克/吨且矿体宽度较大的矿段被认为是“高品位”,对项目的开发具有重要的经济意义,尤其是在矿山运营初期。公司还在研究矿石分选技术,以期提高矿石品位并改善项目经济效益。

=======================

认股权证、期权、内部股权

=======================

https://investorshangout.com/images/MYImages/...302026.jpg

内幕交易更新

https://www.barchart.com/stocks/quotes/SPA.VN/insider-trades

https://www.canadianinsider.com/company-insid...cker=SPA.V

========================

生产基础设施建设融资计划

========================

黄金价格

https://investorshangout.com/images/MYImages/...ology).jpg

https://investorshangout.com/images/MYImages/...ology).jpg

方案 2B - 债务融资 (无XRT选矿技术,处理所有岩石)

https://investorshangout.com/images/MYImages/...ology).jpg

方案 3 - 收购交易

British Columbia Golden Triangle 地区的历史收购交易

https://www.northernminer.com/news/placer-sta...000178407/

Imperial Metals 以每股 $2.45 收购 American Bullion Minerals Ltd.

https://imperialmetals.com/for-our-shareholde...an-bullion

Newmont 以每股 $3.25 收购 GT Gold,交易金额达 $393 million

https://www.newmont.com/investors/news-releas...fault.aspx

澳大利亚黄金和铜生产商 Newcrest Mining 以 每股 $18.5 价格收购 Pretium Resources,交易金额达 $3.84 billion

https://magazine.cim.org/en/news/2021/newcres...e%20region

在 Ontario, Kinross 以 每股 $32 收购 Great Bear Resources, 交易金额达 $1.8 billion

https://www.globalminingreview.com/finance-bu...resources/

==============================

初步经济评估及 NI-43-101 技术报告

==============================

https://investorshangout.com/images/MYImages/...67_PEA.png

初步经济评估 (Preliminary Economic Assessment Economics)

https://spanishmountaingold.com/project/preli...economics/

August 18, 2025 - NI-43-101 技术报告 (Technical Report)

https://spanishmountaingold.com/site/assets/f...-final.pdf

===========================

25家金矿生产商的总体维持成本

===========================

https://www.mining.com/wp-content/uploads/202...31425A.gif

什么是总维持成本 (AISC)?

采矿业(尤其是黄金行业)的总维持成本 (AISC) 包括所有运营成本、维持性资本支出以及维持当前生产相关的其他成本。这包括现金成本、维持性资本支出、一般及行政管理 (G&A) 费用以及环境成本和矿场关闭成本。

总维持成本明细:

现金成本:

这些是采矿和加工的直接成本,包括劳动力、能源、消耗品和特许权使用费(扣除副产品抵扣)。

持续性资本支出:

这些是维持当前生产水平所需的投资,例如设备更换、矿山开发以及维持矿山当前产能所需的其他成本。

一般及行政管理 (G&A) 费用:

这些是与运营公司办公室和其他支持矿山运营的行政职能相关的成本。

环境及关闭成本:

这些包括与环境修复和矿山关闭相关的成本,例如复垦和退役。

勘探费用(维持性):

这些是维持当前生产水平和替换枯竭资源所需的勘探成本。

总维持成本 (AISC) 是一项综合指标,旨在更全面地反映开采一盎司黄金的总成本,而不仅仅是直接现金成本。

=====================

促成建造决策的关键步骤

=====================

Spanish Mountain Gold 表示,生产基础建设会在 2027年做出决定,之后将开始进入为期两年的建设阶段。这一时间安排确保了正在进行的钻探计划、新的矿产资源估算(MRE)和新的初步经济评估(PEA)在2026年上半年完成,以及所有推进项目开发所需的报告和审批手续的顺利取得。新的PEA和MRE是优化项目建设的关键步骤。在做出建设决定之前,完成所有技术报告和监管审批是必要环节。

======

概述

======

矿业项目可以通过替代融资(例如流融资、矿权使用费融资或合资企业)在实现收入之前偿还贷款。这些融资方式的限制比传统债务更少,并且可以使用未来产量或收入作为抵押品,而不是现有收入。其他方法包括获得政府补助和奖励、通过包销协议预售部分未来产量,以及通过发行股票筹集股本。

==============

收入前融资方法

==============

流式协议:一家公司提供前期资本,以换取矿山未来矿产产量的一定比例,通常以折扣价出售。

特许权使用费融资:融资方为项目提供资金,以换取项目未来收入或利润的一部分,这可以被视为对项目潜力的认可。

合资企业:与其他矿业公司或投资者合作可以分摊成本,分散财务负担。

包销协议:将未来矿产产量的一部分预售给买家可以获得前期融资,并使贷款方对项目潜力充满信心。

政府资助:政府和开发银行有时会为符合经济或环境目标的项目提供赠款、贷款或税收优惠。

股权融资:通过发行股票筹集资金通常被认为是早期项目最简单的途径,因为它避免了债务融资的复杂性和严格要求。

这些方法的优势:

非稀释性(针对矿流/特许权使用费:这些选择不会稀释公司原有股东权益。

灵活的条款:矿流和特许权使用费结构比传统银行债务更灵活、限制更少,允许定制还款方案。

市场信心:矿流和特许权使用费等协议可被视为市场对项目的认可,从而可能增强投资者信心。

=========

盈利前景

=========

Spanish Mountain Gold 近期更新的初步经济评估 (PEA) 显示其经济前景良好,基准情景下净现值 (NPV) 为 10 亿加元,内部收益率 (IRR) 为 18.2%,随着金价上涨,净现值 (NPV) 和内部收益率 (IRR) 可能分别升至 23 亿加元和 32.0%。尽管该公司仍处于早期开发阶段,但该项目的传统露天开采、铣削作业、基础设施使用权以及具有施工和运营经验的新管理团队为其潜在的成功做出了贡献。

支持盈利能力的因素:

良好的经济效益:初步经济评估 (PEA) 预计,该项目将带来可观的财务回报,税后净现值 (NPV) 为 $1 billion,内部收益率 (IRR) 为 18.2%,基准金价为 2,450 美元/盎司;现货金价为 3,300 美元/盎司时,回报将更加可观。

强大的资源信心:经济分析基于高度的资源信心,涵盖了已探明和已指示的资源量,这些资源量是采矿项目成功的关键。

经验丰富的管理层:自 2022 年起,公司组建了新的董事会和管理团队,在项目管理、建设和运营方面拥有数十年的经验,为公司制定生产决策奠定了基础。

发达的基础设施:该项目将受益于不列颠哥伦比亚省中部完善的基础设施,包括公路交通便利以及毗邻威廉姆斯湖市的优势,从而降低运营复杂性和成本。

战略项目设计:该公司计划采用传统的露天开采和铣削作业,这是一种低风险的方法,比地下采矿更简单。

信息来源

https://spanishmountaingold.com/news/2025/spa...scal-2025/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

繁體中文

Barkerville是位於 British Columbia Cariboo 地區的一座曾經繁榮的礦業小鎮,距離 Spanish Mountain Gold 以北50公里,它開啟了舉世聞名的卡里布淘金熱。

https://www.google.ca/maps/dir/Barkerville,+B...FQAw%3D%3D

影片長度:5分鐘

https://www.youtube.com/watch?v=XGfM7Ya1ulQ

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

截至5月1日星期五,每股面值 $0.25 的認股權證持有人僅剩19個交易日來行使他們持有的7,411,308份認股權證,這些認股權證將於5月29日星期五到期。如果10天平均收盤價超過 $0.30,則可能提前到期。行使這些認股權證將為公司帶來額外的 1.852 million。

認股權證、選擇權和內部人士持股

https://investorshangout.com/images/MYImages/...302026.jpg

SPA.V 週線圖

https://stockcharts.com/sc3/ui/?s=SPA.V&p...2963243620

============

最新新聞稿

============

正如執行長 Peter Mah 所承諾的那樣,未來的融資將採用非稀釋性方式,與 Wheaton Precious Metals 的特許權使用費融資就是一個先例。

2026年4月21日 - Spanish Mountain Gold 宣布以 US$55 million (约C$75 million)的價格向 Wheaton Precious Metals 出售 1.5% 的礦權使用費。

https://spanishmountaingold.com/news/2026/spa...5-million/

2026年5月1日 - Spanish Mountain Gold 宣布完成首期矿产资源融资并收到 US$22.5 million (约 C$30 million)

https://spanishmountaingold.com/news/2026/spa...5-million/

要点:

- 首期款项 US$22.5 million 来自 Wheaton 已完成支付。

- 工程完成 60,000 meters 鑽探後,Spanish Mountain Gold 將收到第二筆款項 US$12.5 million。

- 專案獲得 British Columbia 省環境評估法規定的礦場建設、開發和營運許可後,Spanish Mountain Gold 將收到第三筆款項 US$20 million。

WPM.TO 週報

https://stockcharts.com/sc3/ui/?s=WPM.TO&...8609492691

Wheaton Precious Metals 網站

https://www.wheatonpm.com/news/default.aspx

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

關於 Wheaton Precious Metals (WPM.TO)

Wheaton Precious Metals 是全球領先的貴金屬串流媒體公司。與傳統礦業公司不同,Wheaton 並非直接擁有或經營礦場。相反,它採用“串流媒體”模式,作為專業融資機構,為礦業公司提供前期資金,用於建造或擴建礦山。

這是 Wheaton 的商業模式:

https://www.wheatonpm.com/about/Our-Business-...fault.aspx

流式交易協議:Wheaton 透過預付融資,獲得從這些礦場購買未來一定比例貴金屬產量(具體而言是黃金、白銀、鈀金和鈷)的權利,購買價格可以是低廉的固定成本或浮動成本。

資產組合:Wheaton 擁有高品質的資產組合,這些資產壽命長、成本低,在全球擁有超過23個營運礦場和25個開發案的協議。

收入來源:公司透過出售透過這些流式交易購買的金屬來獲得收入,使投資者能夠從商品價格上漲中獲利,而無需承擔傳統採礦相關的營運風險(資本支出、環境風險或政治風險)。

重點領域:雖然 Wheaton 專注於貴金屬,但他們的協議通常是與大型多金屬礦山(例如銅礦)簽訂的,在這些礦山中,貴金屬是副產品。

Wheaton 與 Spanish Mountain Gold 達成的協議是支付該公司淨收入的1.5%作為特許權使用費。該公司主要礦產為黃金和白銀。 2024年的鑽探計畫顯示,便攜式X射線螢光光譜儀(XRF)分析表明,該礦藏可能蘊藏著包括鈦(Ti)、錳(Mn)、鎂(Mg)和鎳(Ni)在內的關鍵元素。該公司正在分析這些數據,並計劃在未來的勘探項目中進一步研究這些元素的潛力。此外,該礦藏還蘊藏方鉛礦、閃鋅礦、黃銅礦和黃鐵礦等賤金屬。

Wheaton Precious Metals 成立於2004年,總部位於 Vancouver, 是串流媒體領域的領導者。

現金餘額 (2025年12月31日):US$1.15 billion

資產:US$1.2 billion

負債:US$0.43 billion

2025年銷售額: US$2.3 billion

2025年銷售成本:US$0.64 billion

毛利:US$1.67 billion

稅後淨利: US$1.47 billion

流通股數:454 million

每股盈餘: US$3.24

本益比:60

股價:C$198

市值:C$89.9 billion

=========================

XRT礦石分選技術進度新聞

=========================

Spanish Mountain Gold 在其 Phoenix 礦床 的第一階段XRT礦石分選試驗中取得了非常積極的成果,該技術預計將原礦(ROM)品位提高一倍,同時剔除50%至70%的廢石。試驗結果顯示黃金回收率達85%至92%,目前正在進行第二階段的大宗樣品測試,以期在2026年進行經濟性研究。在第一階段取得正面成果之後,第二階段正在與主礦床並行評估100公斤的大宗樣品,旨在優化分選演算法。該計劃旨在大幅縮小擬建選礦廠的規模,並降低專案的初始資本支出 (CAPEX),相關成果預計將於 2026 年納入更新後的經濟評估。合作夥伴 ABH Engineering Inc. 和 OrePortal Technologies Ltd. 正在進行顆粒和散裝分選分析。公司計劃透過提高礦石品位來提升專案經濟效益,從而在 2027 年做出建設決策。

==========

近期活動

==========

***** 金屬投資者論壇 (MIF)(2026 年 5 月 8 日至 9 日)將在加拿大 BC 省 Vancouver 的 JW Marriott Parqr 酒店舉行。39 Smithe St, Vancouver, BC V6B 0R3, Canada.

https://metalsinvestorforum.com/metals-investor-forum/

https://www.google.ca/maps/place/JW+Marriott+...FQAw%3D%3D

https://www.google.ca/maps/@49.2751365,-123.1...FQAw%3D%3D

***** 新的初步經濟評估 (PEA) 以及 2025 年秋季鑽探計畫的新礦產資源估算 (MRE) 將於 2026 年 5 月或 6 月發布。 2026 年的 PEA 將顯示礦場建設資本支出大幅減少,礦產資源估算 (MRE) 大幅增加,以及選礦廠黃金原料品位大幅增加。

***** Spanish Mountain Gold 將參加於 6 月 2 日至 4 日在加拿大 Quebec 省 Quebec 市舉行的年度礦業投資盛會 (THE Event)。

執行長 Peter Mah 在 2025年 礦業投資活動(6月3日至5日)上介紹了 Spanish Mountain Gold。

https://www.youtube.com/watch?v=9MDABJPTEFU

***** 60,000公尺鑽探計畫、可行性研究、施工決策

摘自2025年12月31日年度報告管理層討論與分析第11頁:“公司目前的戰略重點仍然是優化、降低風險並推進其西班牙山金礦項目,力爭在2027年底前做出建設決策。隨著2025年初步經濟評估(PEA)的完成,公司將直接進入可行性研究(FS)階段。公司已就2025年第四季度開展可行性研究征求方案,並於近期將牽頭單位授予 BBA Engineering Ltd.。在此期間,公司將與 BBA 合作,於2026年上半年 發布PEA更新報告,其中將考慮鳳凰礦床礦化的潛在新增情況、2025年冬季和秋季鑽探計劃的結果、礦石分選的優勢以及更高的長期黃金產量預測。公司預計在未來十二個月內至少鑽探60,000米,直至項目投產。”預計於 2027 年進行可行性研究。此次鑽探將包括選礦廠和尾礦庫設計所需的地質技術和水文鑽探及測試工作"。

https://spanishmountaingold.com/site/assets/f...4-2025.pdf

=================================================

Spanish Mountain Gold 正在逐步接近可行性和礦山建設決策

=================================================

2026年2月27日 - Spanish Mountain Gold與Metso Canada Inc.簽署諒解備忘錄

https://spanishmountaingold.com/news/2026/spa...anada-inc/

Metso Canada 服務(視頻)

https://www.youtube.com/watch?v=wgiF9uZqDsE

Metso Canada 網站

https://www.metso.com/corporate/sustainabilit...-offering/

Metso Canada(前稱Metso Outotec) 是一家技術供應商,為提供多家公司採礦設備例如破碎機和磨機, 包括位於 British Columbia Cariboo 地區 的 Blackwater Mine。作為一家全球領先的工業公司,Metso Canada 在骨料、礦物加工和金屬精煉行業的可持續技術、端到端解決方案和服務方面處於領先地位。該公司致力於通過其產品提高客戶的能源和水資源利用效率,提升生產率並降低環境風險。破碎、篩分和研磨是其核心業務。Metso 總部位於Espoo, Finland。截至2025年底,Metso在全球約50個國家擁有近18,000名員工,2025年的銷售額約 5.3 billion 歐元。

Metso業務的關鍵方面:

骨料:為採石和建筑行業提供破碎和篩分設備(移動和固定)。

礦物加工:提供採礦技術,包括磨礦機、分離、過濾和尾礦管理。

金屬精煉:提供金屬加工解決方案。

服務與磨損件:提供廣泛的售后服務、備件和磨損件,以優化設備性能。

可持續性:專注於“積極地球”解決方案,旨在減少客戶運營中的能源和水消耗。

======================================================

Spanish Mountain Gold - 展望未來 ( 追隨 Blackwater Mine 的足跡 )

======================================================

Blackwater Mine - Artmis Gold 擁有,位於西班牙山黃金 以西250公里,Prince George 以西南160公里。

Google Blackwater Mine 地圖

https://www.google.ca/maps/place/Blackwater+M...FQAw%3D%3D

Artemis Gold 股價 (ARTG.V)

https://stockcharts.com/sc3/ui/?s=ARTG.V&...8838982129

該礦為露天金銀礦,礦山壽命為22年,選礦廠日處理量為16,000噸,可於第6年擴建至33,000噸,在第11年擴建至55,000噸。該礦已探明黃金儲量為 8 million 盎司,白銀儲量為62.2 million 盎司;概略資源量為11.7 million 盎司黃金,白銀儲量為122.4 million 盎司。

2022年6月,在第一階段工程建設期間,Metso 向 Blackwater Mine 交付了一台Superior MK-III 4265型18兆瓦一級旋回破碎機、HP900型圓錐破碎機(二級和三級)以及一台14兆瓦Premier球磨機。此次交付還包括板式給料機、泥漿泵、水力旋流器和RockSense粒度分析儀。

https://investorshangout.com/images/MYImages/...erMine.jpg

第一階段營運成本為 312 million 加元,其中包括授予Sedgman公司的工程、採購和施工(EPC)費用。

Sedgman 是全球領先的礦物加工和基礎設施解決方案供應商,提供從設計、工程到施工和營運的全流程服務。他們專注於煤炭、賤金屬/貴金屬和關鍵礦物,致力於為全球礦業客戶最大限度地提高回收率、優化效率並管理尾礦。

https://www.sedgman.com/

Artemis Gold 也向 Finning Canada 訂購了價值 134 million 加幣 Blackwater Mine 的第一階段開發所需主要採礦設備,這是初期資本支出的重要組成部分。這批運輸和裝載設備包括卡特彼勒卡車和挖土機,第一期計畫總投資預計為 730 million 至 750 million 加元。

https://www.finning.com/en_CA.html

礦場建設於2023年啟動,歷時22個月完工,金銀礦體於2025年初開始澆鑄。作為加拿大最大的黃金開發案之一,該礦採用100%電氣化設計,旨在打造低排放的露天礦場。礦山於2025年5月30日正式投產。

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso Superior MK-III 4265 型一級旋迴式 18MW SAG 磨機破碎機 (將大塊礦石破碎成小塊礦石)

https://www.youtube.com/watch?v=AVLicyiBLo8

Metso Canada 的 Superior MKIII一級旋回破碎機被認為是採礦領域的重大創新,與傳統破碎機相比,其產能提升高達30%,維護停機時間減少高達70%。這款破碎機作為首款高速一級旋回破碎機推向市場,採用創新的數位化自動化技術,配備可旋轉的破碎筒體以延長襯板壽命,並具有卓越的投資效率. 旋回破碎機是傳統礦石破碎法的典範轉移。

旋回破碎機的工作原理是什麼?

https://www.youtube.com/watch?v=IYeOW7UCZAg&t=15s

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso Nordberg HP900 型圓錐破碎機 (將小塊礦石破碎成卵石)

https://www.youtube.com/watch?v=PRLCfhPudG8

圆锥破碎機的工作原理是什麼?

https://www.foremanequipment.com/cone-crushers/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Metso 14MW 球磨機 (將鵝卵石粉碎以提取金銀顆粒)

https://youtu.be/4VmJ0vBRAG4

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

設備合同是通過 Sedgman Canada Limited 促成的,該公司負責工程、採購和施工的管理。

隨后的濕法廠(磨礦和CIL工藝)將運營從建設階段轉變為生產階段。

該地點設有一個完全電氣化的加工設施、一條225千伏的輸電線和一個重要的尾礦儲存設施。

該項目雇用了超過400人,其中有很高比例的本地和土著代表。

設計時考慮了低碳足跡,用電動設備替代傳統燃料進行採礦和加工。

這是一個露天金銀礦,礦山壽命為22年,礦廠處理量為每天16,000噸,6年后可擴展至每天33,000噸,11年后可擴展至每天55,000噸。 它擁有800萬盎司的黃金、6220萬盎司的白銀的探明儲量,以及1170萬盎司的黃金、1.224億盎司的白銀的可能資源。

=======================

Blackwater Mine -資本支出

=======================

Blackwater Mine 第一期工程的初始資本支出(CAPEX)預計在 730 million 加元至 750 million 加元之間。截至2023年12月31日,已支出約389 million 加元,其中預計範圍下限 (615 million 加元)的84%已簽訂合約。

剩餘資本支出:截至2024年3月31日,第一期工程剩餘資本支出預計為 207 million 加元至 227 million 加元。

工程範圍:第一期工程的重點在於興建一座露天礦場及一座年產能為 6 million 噸 的加工廠。

後續第一階段升級(“第一階段A”)

2025年9月,Artemis Gold 宣布計畫升級第一階段選礦廠(稱為第一階段A),目標是在2026年第四季將產能從 6 million 噸/年提升至 8 million 噸/年。

第一階段A資本成本:預計 100 million 至 110 million 加元,將由營運現金流提供資金。

目標:在充分利用第一階段建立現有團隊的基礎上,提高處理量和效率。

2025年12月,Artemis Gold 批准了一項 1.44 billion 加元的第二階段擴建計劃,旨在將年產能從 8 million 噸提升至 21 million 噸。 2026年3月,Metso 向 Blackwater Mine 提供了一台 Superior MKIII型 一級旋回破碎機和多台 Nordberg HP系列 圓錐破碎機,總價值約 39 million 歐元 (45.25 million 加元,42 million 美元)。該項目計劃於2026年第三季動工建設,預計於2028年底前完工。擴建成本將主要透過營運現金流籌集。未來十年,金礦年產量將超過 500,000 盎司。

https://artemisgoldinc.com/news/media-release...water-mine

=================================

Blackwater Mine - 平均金品位和銀品位

=================================

前五年:平均金品位 1.29 克/噸。

后十七年:平均金品位 0.75 克/噸。

銀品位:預計礦山壽命期內平均銀品位為 5.78 克/噸。

儲量:探明和概略儲量總計估計為 334.3 million 噸,金品位 0.75 克/噸,含金量 8 million 盎司﹔銀品位 5.8 克/噸,含銀量 62 million 盎司。

前五年平均年產量:黃金 463,000 盎司,白銀 1.9 million 盎司

======================================================

Blackwater Mine 2025 年黃金平均實際售價, 維持成本, 生產淨利潤

======================================================

Blackwater Mine 在截至2025年12月31日的三個月內(“2025年第四季度”)創下季度黃金產量68,480盎司的紀錄,為其首個運營年度畫上了圓滿的句號,使2025年全年黃金產量達到192,808盎司。該季度黃金產量較上一季度增長12%,主要得益於選礦廠進料品位和加工回收率的提高。

https://www.artemisgoldinc.com/news/artemis-g...6-guidance

https://www.artemisgoldinc.com/news/media-rel...ng-results

根據 Artemis Gold 發布的財務業績,2025 年黃金平均實現售價為每盎司 3,684 美元(每盎司 5,095 加元)。

2025 年第四季度黃金平均實現售價比較高, 每盎司 4,168 美元(每盎司 5,764 加元)。

維持成本 (AISC) 為每盎司 869 美元(每盎司 1,200 加元)。

Blackwater Mine 2025年 淨利潤為每盎司黃金 5095 加元 - 1200 加元 = 3895 加元

2025年 黃金總產量為 192,808 盎司

2025年 生產淨利潤為每盎司 3895 加元 x 192,808 盎司 = 7.5 億 加元

2026年4月9日-Artemis Gold宣布,Blackwater Mine 在2026年第一季生產了 61,923 盎司黃金。該選礦廠處理了1.32 million 噸礦石,礦石品位保持強勁,平均品位為1.59克/噸。公司維持全年黃金產量預期為 265,000 至 290,000 盎司,正利用營運現金流繼續推進1A期擴建工程及2期擴建工程。 2028年底,年處理量將增加至 21 million 噸,是目前產能的三倍,年黃金產量也將超過 500,000 盎司。

=======================

Blackwater Mine 建設視頻

======================

1) 2025年2月 - 空中巡游

https://www.youtube.com/watch?v=ndcRuX42b3U

2) 2025年2月 - 礦業技術

https://www.youtube.com/watch?v=8WfAvX_Nzb4

3) 2025年2月 - 健康與安全

https://www.youtube.com/watch?v=ELbEBpNQMAw

4) 2025年2月 - 完工

https://www.youtube.com/watch?v=fpl3Vjd9slM

5) 2025年4月 - 首次黃金澆鑄於2025年1月進行

https://www.youtube.com/watch?v=E9nFlVjKIe4

6) 2025年5月30日 - 開幕式

https://www.youtube.com/watch?v=MOXjjZcGdYw

7) 2025年12月 - 第二階段:生產擴展

https://www.youtube.com/watch?v=R7xr4kidz4I

=================================================

Spanish Mountain Gold - 透過Gibraltar Mines的一生未來展望

=================================================

https://www.youtube.com/watch?v=yJmanh1uQMQ

Gibraltar Mines - 隸屬於 Tasedo Mines,位於 Spanish Mountain Gold 以西50公裡處

https://www.google.ca/maps/place/Gibraltar+Mi...FQAw%3D%3D

Gibraltar Mines 是加拿大第二大露天銅鉬礦,其主要資源為低品位斑岩型銅鉬礦床,礦物成分包括黃銅礦、輝鉬礦、斑銅礦和赤銅礦。截至2024年12月31日,該礦擁有6.16億噸礦石,銅品位為0.26%,鉬品位為0.008%。

https://stockcharts.com/sc3/ui/?s=TKO.TO&...5512188236

=============================

Spanish Mountain Gold - 公司介绍

=============================

https://spanishmountaingold.com/investors/presentations/

==========

未來展望

==========

Spanish Mountain Gold 的市值遠低於同業。分析師給出的目標價表明該公司被低估,具有巨大的成長潛力, 原因包括即將發布的資源更新報告、潛在的高品位礦藏發現,以及利用現有水力發電資源開發獨特的「綠色黃金」機會。

即將到來的催化劑:新的初步經濟評估和資源估算預計將重新評估該股的價格。

礦化潛力:該項目擁有覆蓋廣泛、品位高的礦化帶,表明未來存在發現金礦的潛力。

綠色黃金機遇:該公司擁有清潔水力發電的渠道,為其帶來了獨特的“綠色黃金”投資前景。

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

財務長 Mark Ruus 介紹 Spanish Mountain Gold 2026 年 1 月 26 日在 VRIC 舉行(長度:13 分鐘)

https://www.youtube.com/watch?v=YzmLGz1Xhhg

Mark Ruus 在礦業領域擁有近三十年的經驗。他最初在普華永道 (PwC) 工作,之後在 Kinross Gold Corporation、Goldcorp Inc.和 Placer Dome Inc.等領先的黃金礦業公司擔任副總裁和高級副總裁稅務職位。他豐富的經驗和註冊會計師 (CPA-CA) 資格,使其在國內外礦業公司的融資、成本控制、業務效率、合規、稅務問題、併購和財務報告方面擁有廣泛的知識。

=============================

Spanish Mountain Gold 的戰略轉變

=============================

審計師更換和領導層過渡作為2026年增長的催化劑

- Spanish Mountain Gold 更換審計師並任命新財務總監,以加強2027年建設決策的治理

- 新審計師 BDO 和 Kim Leroux 的專業知識旨在加強不列顛哥倫比亞省的財務監督和原住民參與。

- 運營准備包括更新的資源估算、2025年的鑽探以及XRT技術,以優化黃金回收並減少碳足跡。

- 戰略舉措應對治理風險和可持續發展趨勢,使公司能夠應對監管和市場挑戰。

採礦行業從勘探階段過渡到開發階段項目需要強有力的公司治理和運營准備。 對於 Spanish Mountain Gold 來說,這家初級勘探公司旨在發展成為新興開發商,最近的戰略舉措——即更換審計師和領導層過渡——表明其有意努力將治理和技術能力與2027年的建設決策時間表對齊。 這些變化,加上運營方面的進展,使公司能夠在資源受限且日益注重可持續發展的行業中,駕馭項目開發的復雜性。

審計師更換:加強發展階段的治理嚴謹性

Spanish Mountain Gold 決定將 Smythe LLP 更換為 BDO LLP 作為其審計師,反映出其在財務監督和信譽方面的戰略轉變。 根據 Business Wire 的一份報告,審計委員會選擇了 BDO,因為其“在與礦業公司合作方面擁有豐富經驗”,這是該公司在推進其西班牙山金礦項目至建設決策時的一個關鍵因素。 這一轉變突顯了公司認識到開發階段項目需要具備行業專業知識的審計師,以應對監管審查和投資者期望。

這一過渡也突顯了資本市場透明度的重要性。 通過在 SEDAR+ 上提交更換審計師通知以及前任和繼任審計師的必要函件,西班牙山黄金 展示了其遵守加拿大証券法規的合規性。 對於投資者來說,這一舉措減少了與缺乏經驗的審計師相關的治理風險,這是歷史上困擾初級礦業公司的一個問題。 BDO 在礦業審計方面的良好記錄也可能促進與貸款人和合作伙伴的更順暢互動,這些貸款人和合作伙伴在承諾大型項目之前通常要求進行嚴格的財務盡職調查。

領導層過渡:Kim Leroux 的任命是治理的勝利

與審計師更換相輔相成的是 Kim Leroux 被任命為財務總監,任命將於2026年1月2日生效。 Leroux 在 DeBeers 和 McEwen Mining Inc.的背景帶來了深厚的礦業金融專業知識,這與公司的運營目標相一致。 值得注意的是,她在第一民族關系管理方面的經驗為公司治理增添了一個關鍵維度,特別是在不列顛哥倫比亞省,在那裡社區參與對項目許可和社會運營許可証至關重要。

從兼職合同首席財務官 Mathew Lee 過渡到 Leroux 的全職領導角色,也解決了初級礦業公司常見的一個弱點:財務管理不一致。 通過確保在2026年第一季度進行無縫交接,公司在最小化運營中斷的同時,也為管理資本密集型的可行性研究和基礎設施規劃階段做好了准備。 勒魯對“開發和實施流程和系統”的關注表明了一種以治理為驅動的擴展運營的方法,這對於吸引機構投資至關重要。

運營准備:技術和可持續性驅動的進展

除了治理之外,Spanish Mountain Gold 的運營准備措施同樣引人注目。 到2025年7月完成新的礦產資源估算(MRE)和初步經濟評估(PEA)為后續的可行性研究提供了數據驅動的基礎。 這些研究結合了2025年的勘探鑽探計劃,目標是10,000米,旨在通過在鳳凰區和K區等關鍵目標地延伸礦化來降低項目風險。

加工技術的創新進一步增強了公司在開發階段的准備。 根據《金融郵報》的報道,探索X射線透射(XRT)礦石分選技術——一種提高黃金回收率的技術——展示了優化項目經濟性的積極方法。 同時,與BC Hydro的合作整合可再生柴油和電氣化舉措,突顯了減少項目碳足跡的承諾,這已成為以ESG為重點的投資者日益關注的優先事項。 這些努力與全球礦業去碳化的趨勢相一致,可能會在一個日益受到可持續性指標影響的監管和市場環境中,改善項目的長期可行性。

戰略對齊與未來展望

Spanish Mountain Gold 在治理和運營准備方面的雙重關注為其2027年的建設決策奠定了協同基礎。 審計師更換和領導層過渡解決了內部能力限制,而技術進步和可持續發展舉措則應對了外部挑戰,如許可延誤和資本成本通脹。 對於處於開發階段的礦業公司來說,這些因素往往是項目成功與停滯之間的關鍵區別。

然而,風險仍然存在。 2025年的鑽探計劃結果將對驗証礦產資源估算(MRE)的假設至關重要,而可行性研究的延遲可能會將建設決策推遲到2027年以后。 此外,Leroux 將原住民合作伙伴關系整合到項目治理框架中的能力將決定監管審批的速度。 投資者必須密切關注這些裡程碑,但公司的當前軌跡表明其成為生產商的道路結構良好。

結論

Spanish Mountain Gold 在2026年的戰略轉變——從審計和領導層變動到運營創新——展示了開發階段的礦業公司如何減輕風險並提升價值。 通過優先考慮治理嚴格性和技術准備,公司正在為利用黃金行業的長期基本面做好准備,同時應對現代資本市場的ESG要求。 對於投資者來說,問題不再是項目能否推進,而是它能多快執行其雄心勃勃的時間表

新聞參考

https://spanishmountaingold.com/news/2025/spa...scal-2025/

====================================

截至2025年7月3日的礦產資源量估算 (MRE)

====================================

https://investorshangout.com/images/MYImages/...timate.png

高品位K區礦床的資源量未包含在7月3日的初步經濟評估 (PEA) 中。

=============================

K區非官方估算的黄金资源量估算

=============================

截至3月10日

https://investorshangout.com/images/MYImages/...K-zone.jpg

鑽井區域:

https://investorshangout.com/images/MYImages/...argets.png

根據 K 區更新的化驗結果,以及主礦區白銀資源量與黃金資源量之比為 1.5,若K區的噸位至少達到2億噸,與主區相同,K 區在 2025 年 7 月 3 日的初步經濟評估中將新增 4 million 盎司黃金和 6 million 盎司白銀的探明 + 指示資源量。2026 年新的初步經濟評估報告 (PEA) 的新礦產資源估算報告 (MRE) 將顯示已探明和已指示的黃金和白銀資源量(已證實儲量)分別為 8 million 盎司黃金和 12 million 盎司白銀。

2025年的鑽探工作持續發現長段高品位金礦表明我們鑽探的區域可能靠近金礦脈網絡,而砂金的來源正是這些金礦脈。這些金礦脈在兩億年的風化作用下崩解,可見的金被腐蝕成細小的砂金。將高品位金礦納入未來的初步經濟評估將顯著改善項目的經濟效益。

“高品位”一詞的含義取決於礦床類型。西班牙山項目主要是一個大型露天礦項目,其礦石品位通常低於窄脈地下礦。在此背景下,品位接近或超過1克/噸且礦體寬度較大的礦石被視為“高品位”,對項目開發具有重要的經濟意義,尤其是在礦山運營初期。公司目前也在研究礦石分選技術,以期提高礦石品位,從而提升項目經濟效益。