Here is an extremely underpriced (trading under ca

Post# of 10

(Total Views: 676)

Posted On: 05/28/2020 9:23:30 AM

Here is an extremely underpriced (trading under cash) and undiscovered biotech stock :

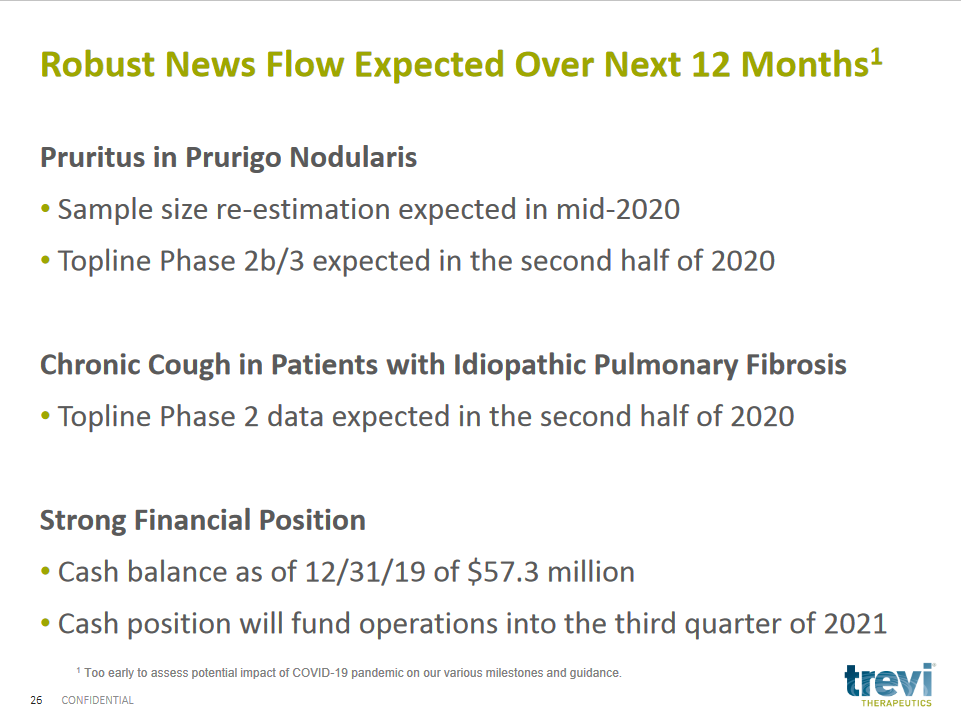

(TRVI-DD) Market Cap $49 million / Cash $53 Million or Cash untill Q4 2021 /Phase 3 Drug targeting Prurigo Nodularis with NO approved treatment for this indication to date a potential Blockbuster .Company has only 17.8 million outstanding shares almost all shares held by Insiders & institutional investors (see below) .This MASSIVE underpriced extreme low float stock could hit $20+ on positive Phase 3 readout and more with FDA approval .GL

Trevi Therapeutics (TRVI)

Market Cap: $49 Million

Cash: $53 Míllion (or untill Q4 2021)

Price: $2.79

Shares Out: 17.8 Million

Company Presentation

https://ir.trevitherapeutics.com/static-files...c102f91b67

Major Shsareholders:

TPG Capital, L.P...6.3M

New Enterprise ...5.9M

Omega Fund ...1.3M

Lundbeckfond ...1.2M

Fidelity ...792.7K

Franklin ...587.3K

Richard King ...347.2K

Meeker (David P)...311.8K

Good (Jennifer L)...206.2K

Sciascia (Thomas R)...193.7K

BMO Capital Markets analyst Gary Nachman initiated coverage of shares of Trevi with an Outperform rating and $15 price target.

The Thesis

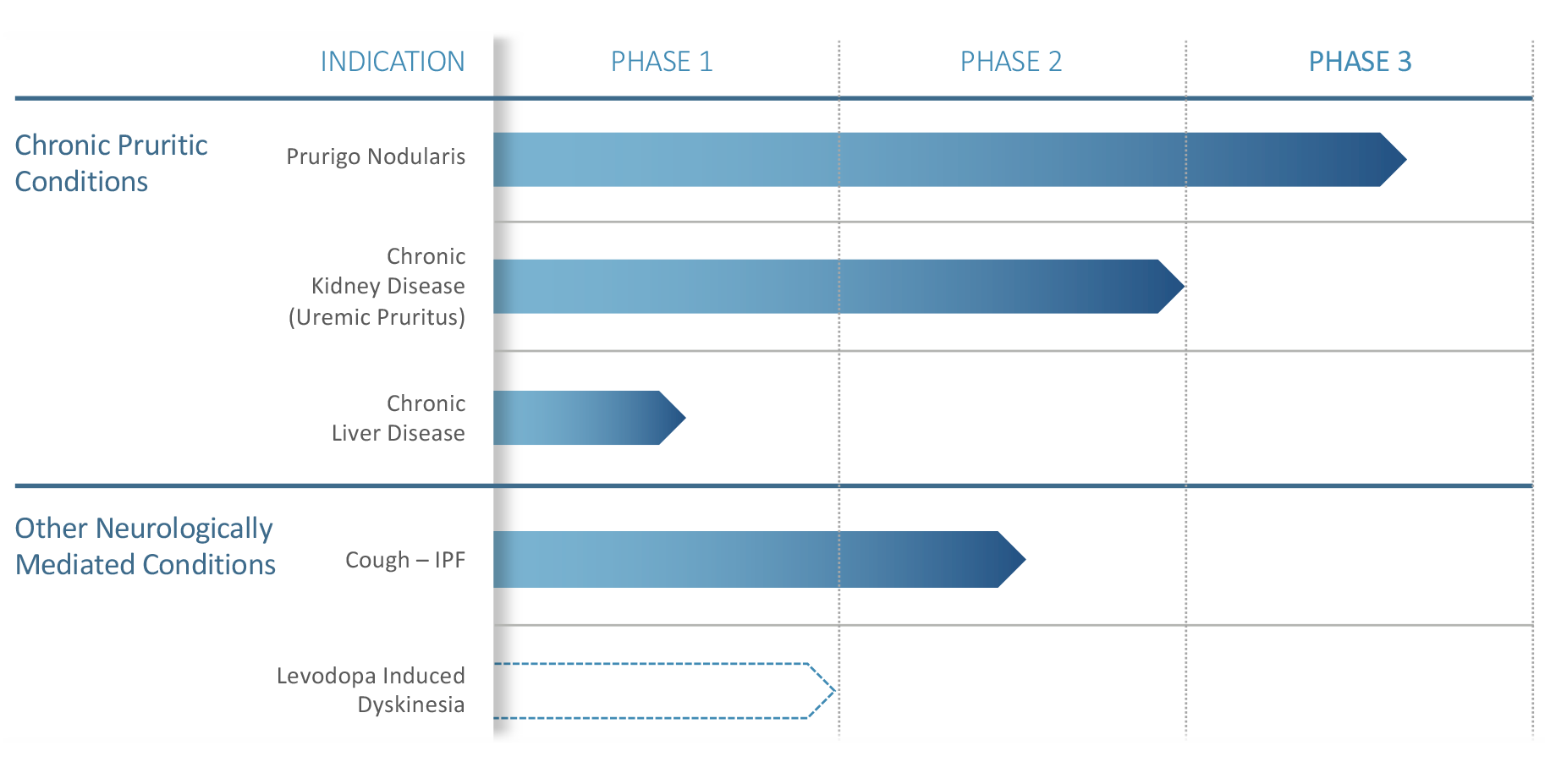

Trevi's key product Nalbuphine ER has a solid track record and substantial evidence supporting its mechanism of treating various chronic pruritus and cough conditions, analyst Nachman said in a Monday morning note.

Nalbuphine ER is an oral formulation of Nalbuphine, an injectable in use for decades to treat pain, and it is the only opioid-based pain drug not scheduled by the DEA, the analyst added.

The pipeline asset has shown positive clinical data in a large Phase 2b/3 trial in uremic pruritus associated with chronic kidney disease, and in a smaller Phase 2 study in prurigo nodularis, the lead indication, the asset achieved statistical significance in a post-hoc analysis for patients who completed the study on the higher dose, Nachman noted.

The analyst said prurigo nodularis is an area of high unmet need with a sizeable market opportunity.

A larger Phase 2b/3 study for the lead indication for which enrollment has begun, according to the analyst, has a good chance of success. Data from the study is expected in the first half of 2020, he added.

"We see a compelling valuation at current levels after recent IPO, with further optionality for Nalbuphine ER in additional indications beyond PN," BMO concluded.

(TRVI-DD) Market Cap $49 million / Cash $53 Million or Cash untill Q4 2021 /Phase 3 Drug targeting Prurigo Nodularis with NO approved treatment for this indication to date a potential Blockbuster .Company has only 17.8 million outstanding shares almost all shares held by Insiders & institutional investors (see below) .This MASSIVE underpriced extreme low float stock could hit $20+ on positive Phase 3 readout and more with FDA approval .GL

Trevi Therapeutics (TRVI)

Market Cap: $49 Million

Cash: $53 Míllion (or untill Q4 2021)

Price: $2.79

Shares Out: 17.8 Million

Company Presentation

https://ir.trevitherapeutics.com/static-files...c102f91b67

Major Shsareholders:

TPG Capital, L.P...6.3M

New Enterprise ...5.9M

Omega Fund ...1.3M

Lundbeckfond ...1.2M

Fidelity ...792.7K

Franklin ...587.3K

Richard King ...347.2K

Meeker (David P)...311.8K

Good (Jennifer L)...206.2K

Sciascia (Thomas R)...193.7K

BMO Capital Markets analyst Gary Nachman initiated coverage of shares of Trevi with an Outperform rating and $15 price target.

The Thesis

Trevi's key product Nalbuphine ER has a solid track record and substantial evidence supporting its mechanism of treating various chronic pruritus and cough conditions, analyst Nachman said in a Monday morning note.

Nalbuphine ER is an oral formulation of Nalbuphine, an injectable in use for decades to treat pain, and it is the only opioid-based pain drug not scheduled by the DEA, the analyst added.

The pipeline asset has shown positive clinical data in a large Phase 2b/3 trial in uremic pruritus associated with chronic kidney disease, and in a smaller Phase 2 study in prurigo nodularis, the lead indication, the asset achieved statistical significance in a post-hoc analysis for patients who completed the study on the higher dose, Nachman noted.

The analyst said prurigo nodularis is an area of high unmet need with a sizeable market opportunity.

A larger Phase 2b/3 study for the lead indication for which enrollment has begun, according to the analyst, has a good chance of success. Data from the study is expected in the first half of 2020, he added.

"We see a compelling valuation at current levels after recent IPO, with further optionality for Nalbuphine ER in additional indications beyond PN," BMO concluded.

(0)

(0) (0)

(0)