For those too lazy to click on a link (LOL) My 2

Post# of 72451

For those too lazy to click on a link (LOL) My 2013 Stock Of The Year: Cellceutix

It is almost sacrilege for a staunch technical analyst like myself to like a stock, as opposed to liking a stock price pattern. But there is one area where I make exceptions and that is biotechnology stocks and in particular, small cap developmental biotechnology stocks. There is probably more leverage in a small-cap developmental biotechnology stock than almost any other sector in the market. There is also just as commensurate leverage on the downside.

The Technical Case

On May 22, 2012 Cellceutix Corporation ( CTIX.OB ) triggered a Buy Signal in its Daily Trend Model and has stayed LONG all of the way up to $1.50, where is it trading in mid-December.

(click to enlarge)

2013 Stock of the Year

By early November, I had seen enough, both in price trend and in the rapid developments in Cellceutix's pipeline, to name it my 2013 Stock of the Year. Whereas the chart above knows nothing about the company other than its stock price progression of higher highs and higher lows, there is a lot going on beneath the surface that merits a closer view of the supporting fundamentals.

The Fundamental Case

From the Cellceutix home page , a description of their leading compound, Kevetrin, now in clinical trials:

Our flagship compound, Kevetrin, is a novel drug that has shown extremely promising laboratory data as a new cancer treatment. Clinical trials have already started at Harvard University's Dana-Farber Cancer Institute and partner Beth Israel Deaconess Medical Center, arguably the pinnacle of cancer research hospitals in the world, to test Kevetrin against advanced solid tumors. Additional studies are being conducted at Beth Israel Deaconess to research Kevetrin in conjunction with two Pfizer multikinase inhibitors as potential new therapies for renal cancer and melanoma. In 2013, we expect to start a clinical trial against blood tumors, sponsored by a European university.

Kevetrin seems to re-activate p53, a crucial protein in tumor suppression that is muted in some form in nearly every cancer. Kevetrin alone could make Cellceutix a multi-billion-dollar company. But, they also have Prurisol, a new treatment ready to start mid-stage clinical trials against psoriasis. Prurisol could also have a billion-dollar price tag hanging from it in the mid-term. Combine the two (not to mention the other six compounds in Cellceutix's portfolio) and although CTIX had a great 2012, 2013 could see the share price move exponentially higher.

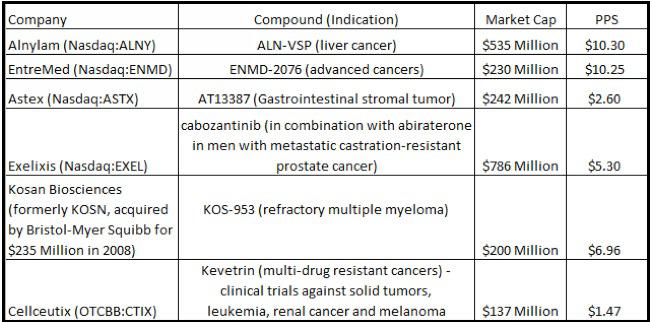

Cellceutix isn't even fairly valued based solely on conducting a clinical trial at Harvard's Dana-Farber Cancer Center and partner Beth Israel Deaconess Medical Center. Take a look at this table:

(click to enlarge)

A simple look shows that Cellceutix is only at about half of the market cap of any other of even the smallest of companies at the time that they began clinical trials at Dana-Farber. A closer look reveals that Cellceutix has actually appreciated to these current levels and was even more undervalued compared to peers, but is making-up ground as trials progress. A more discerning examination shows that Kevetrin being tested against multi-drug resistant solid tumors is a far, far larger market than any of the indications that were tested by other companies. To me, Cellceutix should be valued at a minimum of $2 based on the Dana-Farber/Kevetrin connection, giving it an immediate 33% upside. Further, none of those companies had a drug remotely as exciting or as much of a breakthrough as Cellceutix, so it should already have an even greater value, perhaps $2.50 or so. I suspect as clinical data starts being collected in 2013, Cellceutix's valuation will climb to the top of those valuations and probably much higher.

Remember that Phase I trials are testing for safety and that Kevetrin is only being dosed at low levels once a week. A secondary endpoint of efficacy is still possible, which will send shares soaring, but it is in Phase II that dosing levels are refined. Perhaps the most effective dosing level is several times a week at "x" amount. The drug could be even more effective and, thus, more valuable. With regards to Phase I data that will come in 2013, if Kevetrin is shown to stop tumor growth in its tracks, it would be fair to add $1 per share to the value. If tumor shrinkage is shown, plan on a jump of another $2 per share or so as big pharma is really going to start to hone-in at that point.

The real key to Kevetrin is going to be the biomarker p21 to showcase the activity of p53. If activation of p21 is shown, the p53 connection is validated and Kevetrin goes where no oncology drug has gone before, making it one of the greatest breakthroughs in cancer research ever. If this happens, there is no reason to expect shares of Cellceutix not pressing on $10 per share.

For brevity's sake, I will update everyone on Prurisol at a later date. It is safe to say, though, that based upon acquisition activity in 2012 by major pharmaceutical companies to take possession of early-stage dermatological Prurisol should be worth at least $1.00 per share (at the absolute minimum) for Cellceutix right now and if their Proof of Concept studies in the next few months prove that the drug works, it should be worth at least $3 per share before it even enters a full-blown Phase II/III trial.

The math is actually quite simple. Kevetrin should equal at least $2.50 per share. Prurisol should be worth at least $1.00 per share. That's $3.50 per share as 2012 winds to a close. In the first half of 2013, Kevetrin could be worth $4.50 per share and Prurisol $2.00 per share, putting shares at $6.50. I think that I have explained why CTIX could be at $13 per share by the end of the year if data on Prurisol and Kevetrin continues to accumulate in the frantic and optimistic manner that it has to date.

That Four-Letter Word: Risk

So what's not to love? In a word: RISK. The market's graveyard is littered with developmental biotechnology companies that had a great idea and successful trials, but in the end, no FDA approvable drugs. In fact, there is no contest between small cap biotechnology stocks that made it and those that didn't. As much as I love this sector, it is built upon a foundation of quicksand. What makes Cellceutix different from all of those companies that fell into obscurity? That is the question that values this company at a paltry $150M. My bet is that in the years ahead, Cellceutix will be a billion dollar company. But in the end, it is only an bet, informed as it may be.

What's Next?

2012 saw CTIX shares climb more than 200 percent and that would be considered stellar by any standards, but I believe that 2013 could provide profits on an even grander scale as this company gets the valuation that it deserves.

(0)

(0) (0)

(0)