Data provides evidence that Moody's may upgrade Pl

Post# of 41

Posted On: 01/28/2016 4:15:49 PM

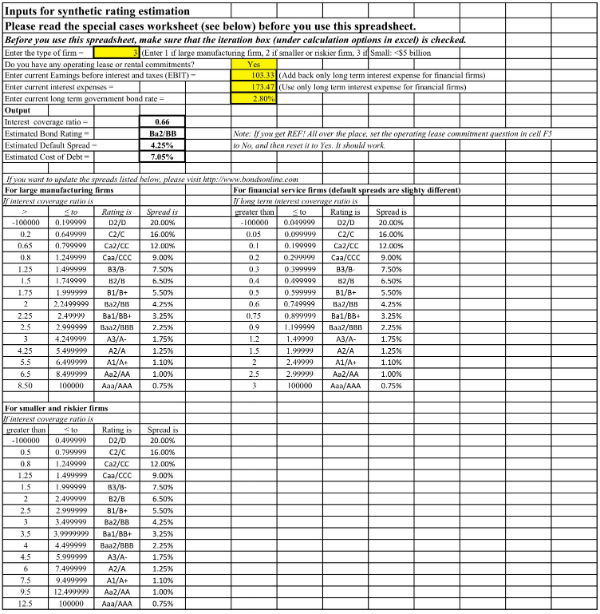

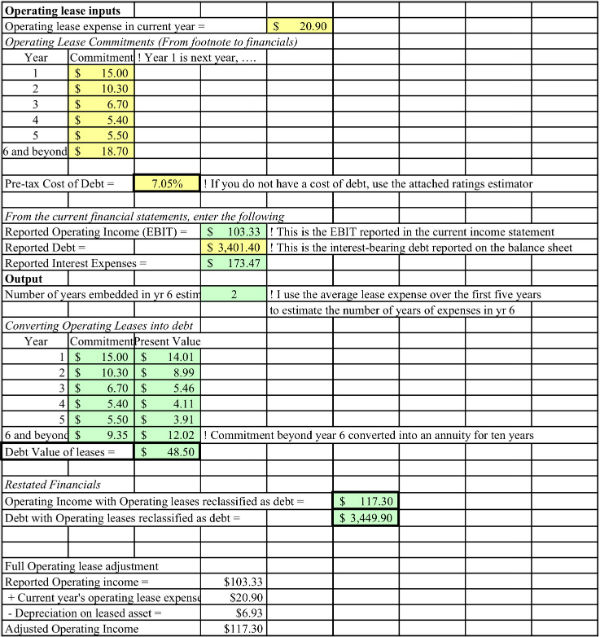

Data provides evidence that Moody's may upgrade Platform Specialty's credit rating from Caa to Ba2//BB, and that Platform has enough cash to cover the remaining interest coverage ratio for the next ten years. With recent exponential revenue increases due to Platforms turnaround efforts in unlocking the value of their acquisitions, it's unlikely that a continuation of the cash burn rate will be needed much longer, especially the next ten years.

The total interest being paid on all long term debt is 5.31%.

The total interest being paid on all long term debt is 5.31%.

(0)

(0) (0)

(0)Element Solutions Inc. (ESI) Stock Research Links

"The more numerous any assembly may be, of whatever characters composed, the greater is known to be the ascendancy of passion over reason." - Federalist no. 58